Earnings before Interest and Taxes (EBIT) to Enterprise Value (EV) is truly the 80/20 valuation ratio when it comes to quantitative investing.

It will nearly always give you the highest returns

You can compare it to any single value ratio, over most time periods, and it will nearly always give you the best returns of any ratio you care to test.

In this article I show you, through back tests, why EBIT to Enterprise Value is a great investment strategy for you to follow as well as how (step by step), to implement it in your portfolio.

EBIT to Enterprise Value = Earnings Yield

In the Quant Investing stock screener we call EBIT to Enterprise Value Earnings Yield and I will use the both terms in this article - just so you know Earnings Yield = EBIT to Enterprise Value.

Returns of EBIT to EV

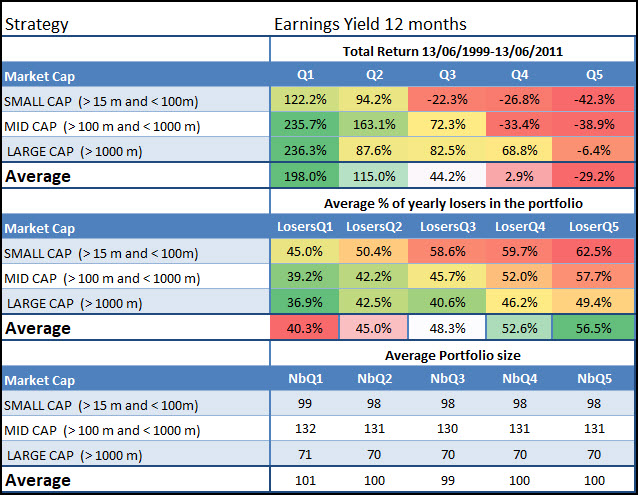

Here are the back tested returns you could have earned if you used and EBIT to Enterprise Value strategy to invest in Europe over the 12 year period 13 June 1999 to 13 June 2011.

Source: Quantitative Value Investing in Europe: What works for achieving alpha

Q1 (Quintile 1) represents the cheapest 20% of companies in terms of EBIT to Enterprise Value and Q5 (quintile 5) the most expensive.

Best for medium to large companies

As you can see the strategy worked best for medium and large companies.

Before I show you how you can improve this investment strategy first some information on how we tested.

Methodology

We only use historical accounting data and no forecasts. The reason being is that there is ample evidence that forecasts cannot be relied on. For example, in his excellent book, ‘The New Contrarian Investment Strategy’, David Dreman mentioned a study that used a sample of 67,375 analysts' quarterly estimates for companies listed on US stock exchanges.

The study found that the average analysts’ error was 40%, and that the estimates were misleading two-third of the time!

So forecasted numbers are just about useless!

The backtest universe and benchmark

Our backtest universe is a subset of companies in the Datastream database containing an average of about 1500 companies in the 17 country Eurozone market during our 12-year test period (13 June 1999 to 13 June 2011).

We excluded banks, insurance companies, investment funds, certain holdings companies, and REITS.

We included bankrupt companies to avoid any survivor bias. Bankrupt companies, or companies that were taken over, returns were calculated using the last stock market price available before the company was delisted.

We excluded companies with an average 30-day trading volume of less than €10 000.

It was not a good time to invest in stocks

The test period was most certainly not a good time to be invested in stocks. The 12-year period we tested included a stock market bubble (1999), two recessions (2001, 2008-2009) and two bear markets (2001-2003, 2007-2009).

In spite of all the substantial movements, over the whole period it was essentially a sideways market, as Vitaliy Katsenelson defined in his book, ‘The Little Book of Sideways Markets’.

Holding periods and quintile tests

Each year all the portfolios we tested were formed on 16 June. We chose 16 June as most European companies have a December year-end and by this date all their previous year-end results would be available in the database.

The annual returns for our back test portfolios were calculated as the 12-month price change plus dividends received over the period. Returns were compounded on an annual basis.

This means each year the return of the portfolio (dividends included) would be reinvested (equally weighted) in the strategy the following year.

The portfolios were all constructed on an equal-weighted basis.

In order to test the effectiveness of a strategy, we divided our back test universe into five equal groups (quintiles), according to the factor we were testing. For example, when testing a low price-to-book (PB) value strategy, we ranked our back test universe from the cheapest (lowest PB) to the most expensive (highest PB) stocks.

The cheapest 20% of companies were put in the first quintile (Q1), the next in the second, and so on, with the 20 % of companies with the highest price-to-book value in the fifth quintile (Q5).

Click here to implement your own EBIT to EV investment strategy NOW!

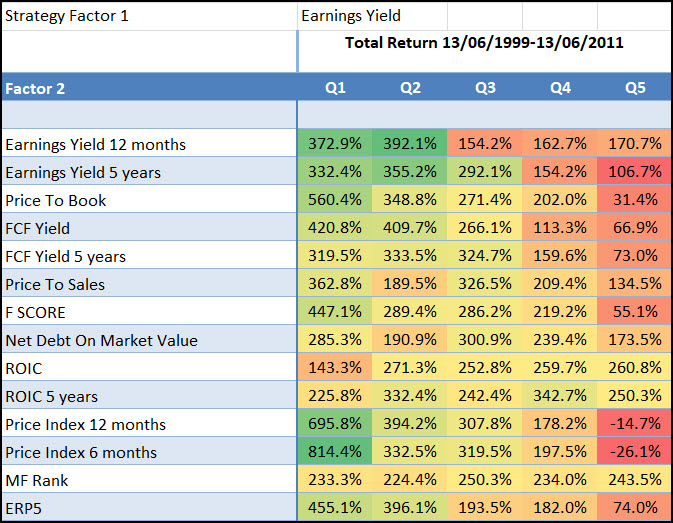

How you can improve the earnings yield investment strategy

You can improve your returns substantially if you combine EY with another ratio or indicator as the table below clearly shows:

Best combination – Momentum

The best way to increase your returns was to combine EBIT to Enterprise Value with Price Index 6 months (6 months momentum) or Price Index 12 months (12 months momentum).

How to implement this strategy in your portfolio

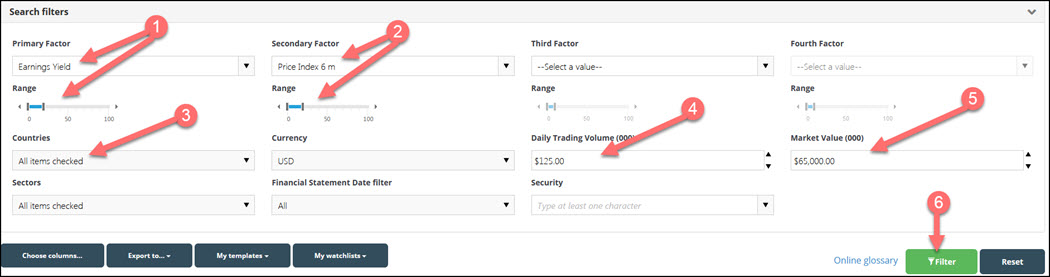

This is how you can implement this strategy in your portfolio using the screener:

- As the first factor or filter select the 20% of companies with highest Earnings Yield (EBIT/Enterprise value)

- As a second factor select the 20% of companies with the highest Price Index 6m (six months price momentum)

- Select the countries where you would like to invest

- Set your minimum trading value per day - $125,000 in the image below

- Select the minimum market value of companies you would like to look for - $65m in the image below

- Click on the filter button to run your screen

Click image to enlarge

In the results table click on the Earnings Yield column heading twice to sort the companies by earnings yield from high to low (the higher the Earnings Yield the more undervalued the company is).

You now have a list of companies that fits this investment strategy.

Limit your losses

We strongly recommend that you use a strategy to keep your losses low. You can read more about that here: Truths about stop-losses that nobody wants to believe

Exact definition – in glossary

You can see the exact definition of all the ratios and indicators in the Glossary

Further reading

You can of course combine EBIT to Enterprise Value with other valuation ratios and indicators. Here is a list of other article you will find helpful:

This outperforms all other valuation ratios (14 year back test result)

This article tells you about Qi Value – which ranks the screener’s whole universe of companies (around 22,000) using the four valuation ratios we have tested with the best results. One of the four ratios is EBIT to Enterprise Value.

A simple ratio beats the world’s best value funds

This article shows you how a simple quantitative value strategy (using just one simple ratio EBIT to Enterprise Value) outperformed the world’s best value investment funds

Is there something like a long term quant value investing strategy?

This article shows you exactly how and why you can implement a simple quant strategy that does not rely on short term rebalancing – in fact the holding period is three to five years.

Quality, value, momentum – the best strategy you have never heard of

This article shows you exactly how to implement the Quality Value Momentum (QVM) investment strategy which contains the best ideas from our research paper Quantitative Value Investing in Europe: What works for achieving alpha as well as all the research we have done since then.

The strategy makes use of EBIT to Enterprise Value and returned an astounding +1142% over 13 years!

Does systematic value investing really work? – Data driven back test

In December 2010 two friends finished an interesting research paper they called Systematic Value Investing: Does it really work?

With this paper they wanted to find:

-

- The best investment strategy in Europe over the 11-years from June 1999 to June 2010

- If small portfolios perform better than large portfolios

- If 30 stock portfolios do better than 50 stock portfolios

What they found was really interesting and I asked them if I can write it up to share with you here.

Use this simple quality ratio to improve your investment returns

This article shows you a simple ratio you could use to increase your returns, irrespective of what investment strategy you follow - also your returns of an EBIT to Enterprise Value investment strategy.

Frequently Asked Questions (FAQs) about EBIT to Enterprise Value Investment Strategy

What is the EBIT to Enterprise Value (EV) ratio and why is it important?

The EBIT to EV ratio, also known as Earnings Yield, is a valuation metric used to assess a company's profitability relative to its overall value. It's calculated by dividing a company's Earnings Before Interest and Taxes (EBIT) by its Enterprise Value (EV).

This ratio is important because it helps you identify undervalued companies that are generating solid earnings relative to their market valuation, leading to potentially higher investment returns.

How does the EBIT to EV strategy compare to other valuation ratios?

The EBIT to EV ratio often outperforms other single valuation ratios. Through extensive back-testing, it has shown to provide higher returns across various time periods compared to other metrics like Price-to-Earnings (P/E) or Price-to-Book (P/B) ratios.

This makes it a great ratio for identifying valuable investment opportunities.

Can the EBIT to EV strategy be used for all types of companies?

While the EBIT to EV strategy works well across different company sizes, it tends to be most effective for medium to large companies.

What are the key steps to implement the EBIT to EV strategy in my portfolio?

To implement this strategy, you should:

- Use a stock screener to filter for companies with the highest Earnings Yield (EBIT/EV).

- Set additional criteria like minimum trading value and market value to narrow down your search.

- Review the list and sort companies by Earnings Yield to identify the best investment opportunities.

- You can also combine your search with a momentum filter (see question below), such as the Price Index over the last 6 or 12 months.

Why should I avoid using forecasted numbers in my investment strategy?

Forecasted numbers are often unreliable. Studies have shown that analysts' estimates can be off by a significant margin, sometimes misleading two-thirds of the time.

Using historical accounting data ensures you are basing your decisions on verified and factual information, leading to more reliable investment outcomes.

How can I further enhance the EBIT to EV strategy to improve returns?

One effective way to enhance this strategy is by combining it with other indicators, such as momentum. For instance, using a combination of high Earnings Yield and high Price Index over 6 or 12 months can significantly boost your returns.

This approach leverages both value and momentum investing principles.

What are the risks associated with the EBIT to EV strategy and how can I mitigate them?

The main risk is that even undervalued companies can experience downturns. To mitigate this, it's crucial to employ a loss-limiting strategy such as stop-loss orders. This ensures that if a stock's price falls below a certain point, it's automatically sold to prevent further losses.

Additionally, diversifying your investments across different sectors and regions can help spread and reduce risk.

Wishing you profitable investing

PS To get this EBIT to Enterprise Value investment strategy working in your portfolio today simply sign up right here.

PPS It’s so easy to put things off, why not sign up right now.

Click here to implement your own EBIT to EV investment strategy NOW!