Last updated: May 2026

By Tim du Toit — 39+ years of quantitative investing experience, author of Quantitative Value Investing in Europe (Amazon). Last updated: April 2026.

Discover a simple yet powerful microcap investment strategy that outperforms the pros. In this article, you’ll learn how small, overlooked companies can lead to big gains, and why this strategy works so well based on real data.

You’ll also get practical step-by-step tips on how to apply this approach to your own portfolio. If you’re looking to increase your returns and stay ahead of the market, this is for you. It’s an easy read that could change how you invest.

This great back tested microcap investment strategy that returned 28.2% annually over 34 years

Related Reading:

How And Why to Implement a Quality Adjusted Value Microcap Investment Strategy - O'Shaughnessy

How To Implement a True Microcap Strategy That Works – Data Driven

In the stock market, you can say that one man’s trash is another man’s treasure.

In the research paper Microcaps — Factor Spreads, Structural Biases, and the Institutional Imperative (August 2017) O'Shaughnessy Asset Management (OSAM) makes a convincing argument that this is true.

Microcap investment strategy — definition:

A quantitative approach that selects companies with a market value of $50–$200 million (microcaps), filtered for quality (high ROIC, low debt, positive free cash flow yield) and ranked by value and momentum factors. O'Shaughnessy Asset Management back-tested this approach over 34 years (1982–2016) and found quality-adjusted microcap value returned 20.3% annually — outperforming large-cap stocks (12%) with a Sharpe ratio of 0.78.

Key findings from the O'Shaughnessy Asset Management research (1982–2016):

- Quality-adjusted microcap value returned 20.3% annually over 34 years — vs 12% for large-cap stocks

- The theoretical value spread (long top decile, short bottom decile) reached 28.2% per year — the headline number

- Quality-adjusted microcap momentum returned 17.8% annually — second best strategy tested

- The winning strategy had the best risk-adjusted return: Sharpe ratio of 0.78

- The back test covered three major market crashes — results held across good and bad markets

- Adding a $100,000 minimum daily liquidity filter improved returns by 0.8% per year — an easy win

The “Junkyard” or Microcap Universe

Microcap stocks, defined as companies with a market value between $50 million to $200 million, have traditionally been seen as a “junkyard” by institutional investors, mainly for two reasons:

- Professional money managers – and most investors - think that microcap companies are high risk weak companies with bad financial health.

- These companies are so small, big investors with billions to invest cannot buy them.

This is really good news!

Because for individual investors like you and me, this “junkyard” of microcap stocks contains jewels that most investors ignore. In fact, O'Shaughnessy found that if you use the right strategy you could have earned 28.2% annually over 34 years!

We show you exactly how to do it – step by step

To find out how you can find the same investment ideas they came up with for your portfolio keep reading for detailed step by step instructions.

What are Microcap companies?

As mentioned microcap companies are defined by O’Shaughnessy to be companies with a market value between $50 million to $200 million. Because they are so small, they are ignored by big investors and have little to no coverage by analysts.

Before we dive into the actual strategies and the returns, let me give you more information about the people behind the research.

Who was the research team?

The research was done by O'Shaughnessy Management, a quantitative investment management firm with around $6.2 billion of assets under management. The seven researchers includes the CEO and six Chartered Financial Analysts (CFAs).

They did this research to show that high returns could be made from investing in microcap stocks.

The researchers are all in-house analysts without any stated conflicts of interest. Since the paper appears to be for the benefit of individual investors, there does not seem to be any potential conflicts of interest. At the moment they do not even have a Microcap fund.

We can trust this research.

What about bias in the back test?

Look-ahead bias

These are experiences researchers so even though they did mention using information that would have been publicly available at the time of investing in a stock, I am sure they automatically did this.

However they did mention that the models constructed “may have been designed with the benefit of hindsight”. I assume this refers to the ratios and indicators they used to select quality microcap companies.

Survivorship bias

Returns could be artificially inflated if companies that went bankrupt were not included in the backtest.

To avoid this, the universe of small and large capitalization stocks consisted of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database with an inflation-adjusted market capitalization of $200 million when they were selected each year.

This is a high quality database where bankrupt companies will most likely also be included. Also if you look for higher quality companies the risk of survivorship bias is smaller because high quality companies do not go bankrupt as often as bad quality companies.

That said when testing Microcap companies over long periods of time the chance of survivorship bias creeping in is high; it all depends on the quality of your data.

Back test period (34 years) - First filter the universe

The research team wanted to make sure that the results they found did not just apply to a few years.

They performed their back tests over a 34 year period from 1982 – 2016, a period with three major stock market crashes in the U.S., so you can know that the strategies have been tested in good and bad markets.

$50 million to $200 million market value

The back test universe started with all microcap companies (market value $50 million - $200 million) trading on U.S. exchanges.

Only US registered companies

When this universe was filtered to include only companies incorporated in the USA it left around 1,300 microcap companies with a total market value of about $100 billion which made up only 0.4% of the total U.S. stock market capitalization.

As you can see this is just about nothing! The total average daily traded value was $700,000.

You can clearly see why large investors have no interest in this market.

Daily average traded value more than $100,000

As transaction costs in the form of market impact and bid-ask spreads are higher for companies with lower daily average volume. For this reason only companies with a minimum daily average traded value of $100,000 were selected.

This should be fine for private investors like us.

This liquidity requirement reduced the back test universe to around 500 companies.

As you will see shortly this universe will further reduced by only selecting quality microcap stocks.

Lower liquidity reduced returns

What surprised me was that by choosing only companies that had a $100,000 daily average value, average yearly returns improved by 0.8% per year over 34 years – this is substantial.

Screen for quality microcap stocks yourself

The Quant Investing stock screener includes all five quality filters used in the O'Shaughnessy research — ROIC, debt-to-equity, free cash flow yield, 1-year debt change, and change in net operating assets. You can set them up in minutes and run the exact screen described in this article across 22,000+ companies worldwide.

Try the microcap quality screen free

No credit card needed. Cancels automatically after 30 days.

Characteristics of the Microcap Universe

In order to develop the best investment strategy the researchers first wanted to find out just what type of companies are mainly found in the microcap investment universe.

When they just looked at the average 3-year sales growth for both microcap and largecap companies they were roughly the same. However just looking at the averages was not helpful because there was much wider range in sales growth for microcap stocks than for largecap stocks.

With further analysis the researchers divided microcap stocks into the following three categories:

- Steady State Firms

- New Ventures

- Fallen Angels

Steady State Firms

59% of these microcaps were ‘steady state’ firms that are defined as companies that had a steady market capitalization of $50 - $200 million for over 3 years. Many of these steady state firms are commercial banks and thrift stores.

Partly due to the low volatility and high returns of banks, steady state firms had the highest average return of the 3 categories at 10.1% annually.

New Ventures

These companies represented about 25% of the microcap universe, and were new companies that just began generating sales. These were often biotechnology or software start-ups recently increased their market capitalization to between $50 - $200 million.

This was the worst performing category with the highest volatility out of all 3 groups. New ventures returned only 4.7% annually with 27.8% volatility.

Fallen Angels

Fallen angels were the smallest group of companies that made up only 16% of the microcap universe. These companies are defined as former largecap companies that have hit hard times and have declined in market value to below $200 million.

Fallen angels delivered an average return of 8% with a volatility of 27.4%.

How to Find Quality Companies in the “Junkyard”

The microcap universe is littered with companies that are not profitable, generating negative cash flow, and are taking on unsustainable amounts of debt.

These are companies you want to avoid and that is why the researchers further narrowed the universe by filtering for “quality-adjusted” microcap stocks.

They removed all companies in the bottom 10%

To do this they removed companies that fell in the bottom 10% of the following five ratios or indicators:

1. Change in Net Operating Assets (NOA = Operating Assets - Operating Liabilities)

Change in Net Operating Assets (NOA) is a measure of the level of assets a company needs to run its business. The average change in NOA for our microcap universe was 44.3%, much higher than their largecap counterparts.

Moderate levels of a change in NOA signal a business than can handle organic growth without having to invest large amounts by for example taking on a lot of debt.

The 10% of microcap companies with the biggest increase in NOA were eliminated from the universe.

2. Debt to Equity Ratio

A high debt to equity ratio raises concerns if the company will be able to pay off its debt. The 10% of microcap companies with the highest debt to equity ratio were eliminated from the universe.

3. 1-Year change in debt

The average one year change in debt of the universe was 32.6%. A large increase in debt signals that the business may be struggling to finance its operations from cash the business generates or that it is growing very fast.

The 10% of microcap companies with the largest increase in debt were eliminated from the universe.

4. Return on Invested Capital (ROIC)

Return on invested capital is a measure at how effective a company is at turning capital into profits. A higher ROIC tells us that company management is investing in profitable projects.

The 10% of microcap companies with the lowest ROIC were eliminated from the universe.

5. Free cash flow yield

Free cash flow is the amount of cash from operations remaining after deducting capital expenditure. Free cash flow yield divides this value by the market cap of the company.

A positive free cash flow yield means a company can sustain itself, while a negative free cash flow yield means a company needs money (debt or capital) to have enough cash to stay in business.

The 10% of microcap companies with the lowest Free Cash Flow yield were eliminated from the universe.

The number of companies remaining after filtering for quality was not mentioned.

Yearly re-balancing with equal weight portfolios

The portfolios were re-balanced yearly and the portfolios were equal-weighted.

This means if a $50 million company was 1% of the portfolio, then a $200 million company would also be 1% of the portfolio.

Costs of buying and selling Microcap companies

As you know high costs can quickly make even the most attractive strategy look bad if the cost of implementing it is too high.

Costs you must look out for are:

- commissions,

- market impact,

- Bid-ask spreads.

In the USA commissions are very low and can be generally ignored. Depending on the amount you decide to allocate to this strategy, the market impact will vary.

For private investors like us and the individual investments we make bid ask spreads will be a cost but it should not be a problem.

All performance results did not include transactions costs, investment management fees, taxes, or any other costs.

So What Were the Returns?

First they compared microcap companies to large stocks to see if their adjustments for quality helped returns at all.

Large stocks were defined as American companies with a market capitalization greater than the average capitalization for the total market (currently those stocks above an inflation-adjusted $7 billion market cap).

As you can see all microcap companies did not do better than large companies BUT quality microcap companies did do a lot better.

Quality adjusted microcap companies gave an annualized return of 14.2%, compared to the 12% return by large stocks. This is a huge improvement because remember this is the average yearly return over a 34 year test period!

Backtest period: 1982-2016

Source: Microcaps — Factor Spreads, Structural Biases, and the Institutional Imperative (August 2017).

What Investment Strategies were tested?

Returns of quality-adjusted group of microcap companies were tested using the following investment strategies:

- value,

- momentum,

- financial strength,

- earnings quality, and

- Earnings growth.

The authors did not define the factors or say what ratios they used to select the companies.

Testing the Investment Strategies

The researchers also tested what your returns would have been if you applied various investment strategies to companies grouped by size.

Large cap was defined as $7 billion or higher market value and small cap as ($200 million to $7 billion market value) companies.

The researchers took the top 10% of stocks filtered on a factor (value for example) and subtracted those returns from the annual returns of the lowest 10% of stocks filtered on that same factor. For example, undervalued returns minus overvalued returns.

This difference is the theoretical return you could earn if you went long the stocks in the top decile and shorted the stocks in the lowest decile.

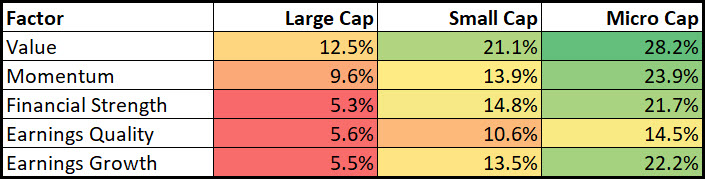

Value and Momentum the most compelling factors

Source: Microcaps — Factor Spreads, Structural Biases, and the Institutional Imperative (August 2017).

The biggest difference was for microcap stocks (the whole universe not just the quality companies) with a value strategy was 28.2% on an average annual basis over 34 years – this is nearly unbelievable.

But this spread assumes that it is practical to short microcap stocks. This is not possible due to liquidity issues, and so the real return you can earn will be lower (but still a LOT higher than just investing in the market).

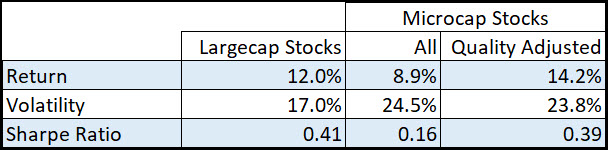

Returns of long only quality-adjusted microcaps

Here are the returns for quality-adjusted microcaps if you used a value and momentum investment strategy (the two strategies with the highest returns from the above table).

These returns were calculated if you went long only – this means buying only the best companies according to the strategy.

Click image to enlarge

Source: Microcaps — Factor Spreads, Structural Biases, and the Institutional Imperative (August 2017).

Quality adjusted Microcap Value won – BY FAR

As you can see the winning strategy, by far was quality adjusted Microcap value.

Not only did it have the highest average return of 20.3%, over 34 years from 1982 – 2016, the volatility of the strategy was not much more than that of Large Cap stocks. This means they had the highest risk adjusted returns – the highest Sharpe Ratio of 0.78.

The second best strategy – with a bit lower returns (17.8%) and slightly higher volatility was quality adjusted Microcap momentum. It was also the strategy with the second best risk adjusted return.

The perfect strategy for you and me

I hope these results convinced you that quality adjusted Microcap companies are definitely worth looking at.

Just think about it:

- They perform better than large companies,

- Large investors cannot invest in them

which means they are the ideal investment strategy for small investors like us.

Summary - A great strategy for you to implement

Now we get to the interesting part of this article – where I show you exactly how to implement the results of this research in your portfolio.

This is what we learned from the research:

- Value and momentum quality-adjusted microcap stocks deliver the highest returns relative to risk.

- Although the researchers did not touch on it in the paper, you can earn great returns by combining value and momentum in one strategy. This means looking for undervalued companies (value) with an upward moving share price (momentum).

- Filtering stocks based on earnings quality or financial strength does not help returns much so we can leave them out. Remember they were the factors that added the least to returns – see the above table.

- Finally avoid large cap stocks and stick to the quality adjusted microcap universe.

- This is the space where small investors like me and you have a big chance at earning great returns and outperform the market and big money managers.

How to Implement this Microcap Strategy

Everything you need to implement the best ideas from the research paper is already built into the Quant Investing stock screener.

This is how you do it.

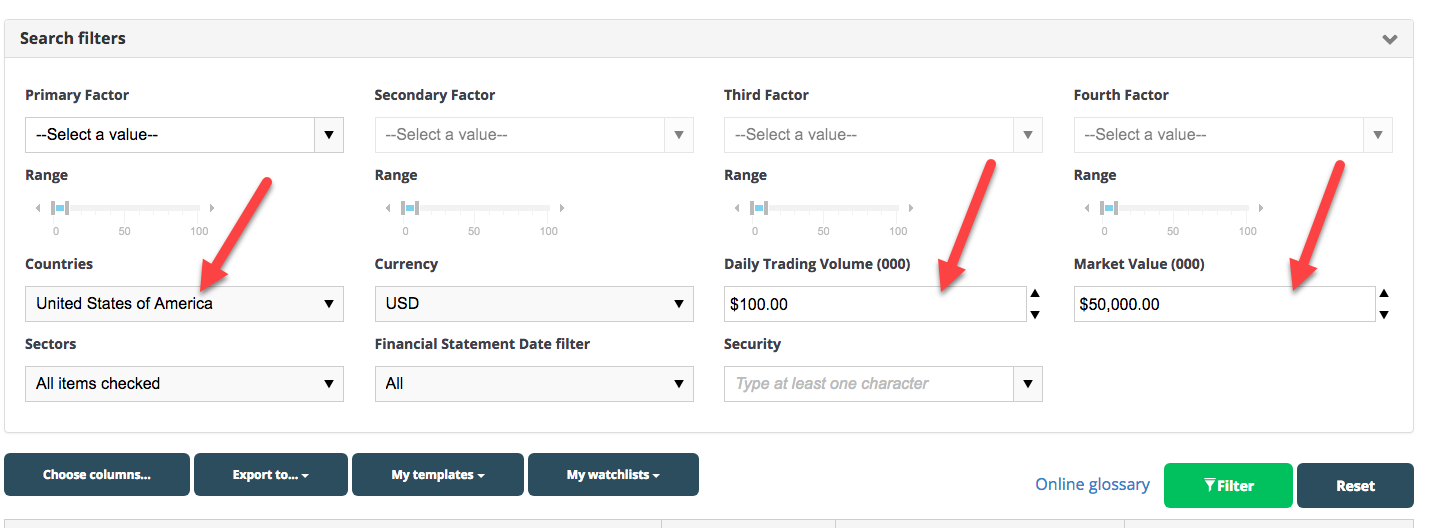

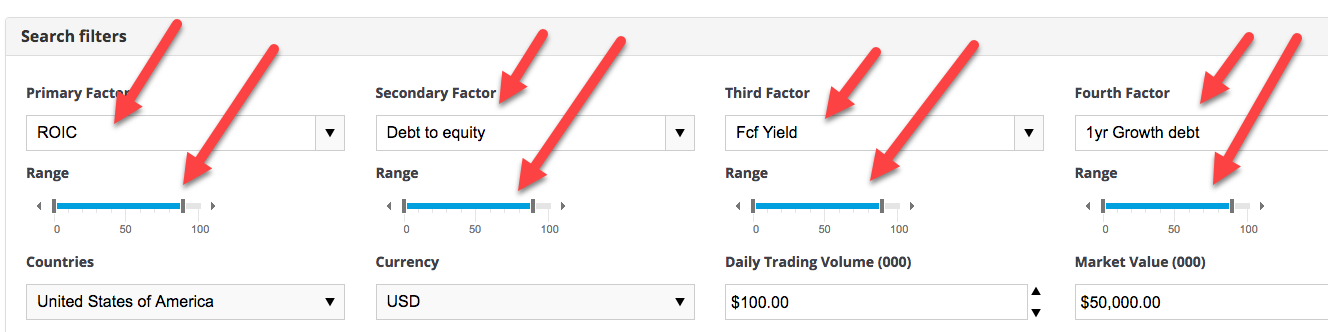

First select Microcap Stocks in the United States

Our edge as small investors is in the microcap universe so we want to make sure that we are selecting only small companies.

For this, we first set the minimum market cap as $50 million.

Since these companies are small, you make sure ensure that you can easily buy them so set at least a $100,000 daily trading value.

The strategies tested in the paper only used US stocks, so we only selected companies registered in the USA. You can of course select all the countries where you like to invest.

Click image to enlarge

Next, we set the maximum market cap as $200 million to make sure we don’t get small or large cap stocks.

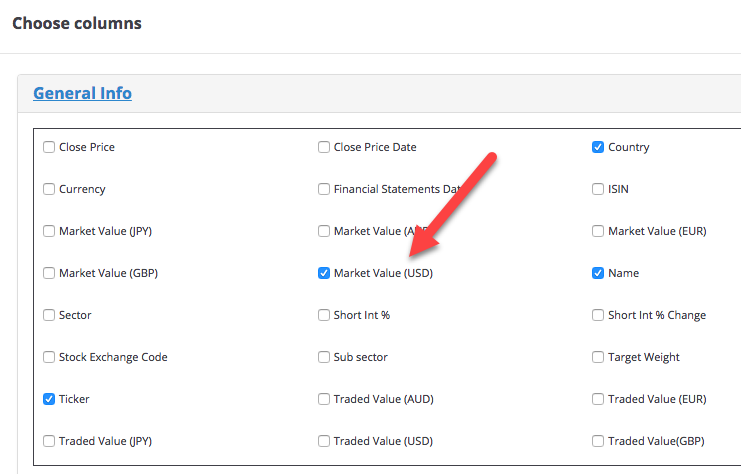

Click the Choose columns button then select Market Value (USD).

Then in the column filter type in 200,000 (remember numbers are entered as thousands), then click on the funnel icon and select smaller than.

Adjusting your Microcap Universe for Quality

Remember we are looking for the jewels among the junkyard, so we need to choose only quality-adjusted microcap stocks.

We do this using the following 4 ratios and indicators:

- Return on Invested Capital

- Debt to Equity

- Free Cash Flow Yield

- 1 Year Debt Growth

Remember with these settings you want to remove the worse 10% of companies, just like the researchers did. That is why you should set the sliders to ignore the bottom 10% of companies in each case.

Click image to enlarge

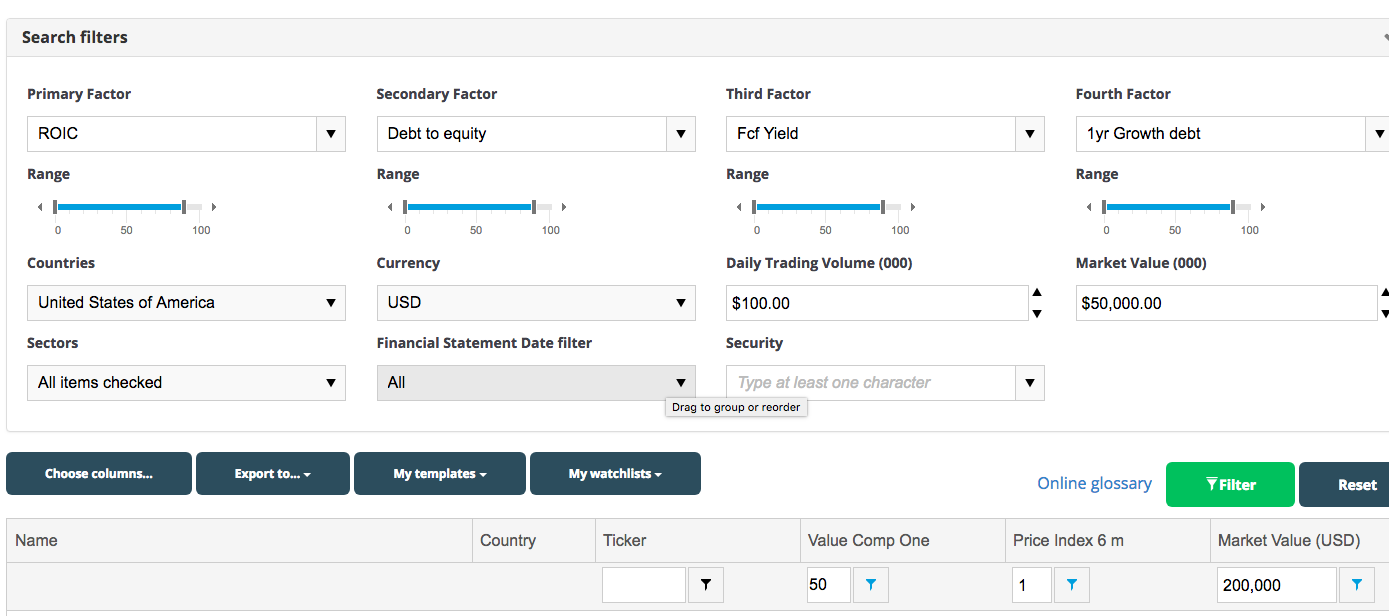

Select stock with Value and Momentum

O’Shaughnessy found that value and momentum stocks produced the best return. In order to select stocks that are at a bargain and exhibit positive momentum, we use:

- Value Composite One and

- Price index 6 month

The Value Composite One is a group of value indicators that was developed by O’Shaughnessy himself. The scale ranges from 0 -100, and lower numbers represent undervalued companies.

The price index 6 month is calculated by taking the current share price and dividing it by the share price 6 months ago.

We set Value Composite One to less than or equal to 50. We set 6 month price index to greater than or equal to 1.

You can sort Value Composite One from low to high (to do this simply click on the column heading), so the most undervalued companies appear first.

You are done.

The list of stocks the screener produces should all be quality-adjusted microcap stocks with good value and strong positive momentum.

This is what your final screen should look like.

Click image to enlarge

That is all you need to do

That is all you need to do to enjoy the returns that big institutional investors cannot touch and only dream about!

Wishing you profitable investing

Find your own quality microcap ideas with the screener

Everything shown above — market cap filters, the five quality ratios, Value Composite One ranking, and 6-month price momentum — is built into the Quant Investing stock screener. The free demo gives you full access to run this screen yourself across the global microcap universe.

Start finding quality microcap stocks free

No credit card needed. Cancels automatically after 30 days.

Frequently Asked Questions

1. What is a microcap stock?

A microcap stock is a company with a market value between $50 million and $200 million. O'Shaughnessy Asset Management found approximately 1,300 US microcap companies in their 34-year back test (1982–2016), with a combined market value of around $100 billion — just 0.4% of total US market capitalisation. Because they are too small for institutional investors to take meaningful positions, they are structurally under-researched and often mispriced.

2. Why should I invest in microcap stocks?

Microcap stocks are less covered by analysts, offering opportunities for individual investors to find undervalued companies with high growth potential.

3. Is investing in microcap stocks risky?

Yes, microcap stocks can be volatile and risky, but by focusing on quality companies you can reduce risks and improve returns.

4. How do I identify quality microcap stocks?

Look for companies with strong fundamentals, such as low debt, positive cash flow, and high returns on invested capital.

5. What strategies work best with microcap stocks?

O'Shaughnessy Asset Management found that value and momentum factors produced the largest return spreads in the microcap universe. Quality-adjusted microcap value returned 20.3% annually over 34 years; quality-adjusted microcap momentum returned 17.8%. Combining both factors in one screen — buying undervalued microcaps with rising price momentum — is the approach with the strongest long-term evidence.

6. How much should I allocate to microcap stocks in my portfolio?

Allocation depends on your risk tolerance. Since microcaps are riskier, a smaller portion of your portfolio might be wise.

7. Can I beat professional investors with microcap stocks?

Yes, due to their size and lack of coverage, microcaps can offer opportunities to outperform the market and even professional investors.

8. How often should I review my microcap investments?

Yearly rebalancing is recommended to adjust for changes in company performance and market conditions.

9. What are the transaction costs associated with microcap stocks?

Costs like commissions and bid-ask spreads can impact returns, but they are generally manageable for private investors.

10. How long should I hold microcap stocks?

A long-term approach, yearly rebalancing, holding through market cycles, and stopping losses before they get too big, is best for realizing the full potential of microcap investments.