In spite of the markets nearly everywhere being quite expensive you could have earned up to 20.5% so far in 2017 if you chose the best performing investment strategy.

How the markets performed

Before we look at what strategies worked and what did not let’s first look at what the markets did in the first half of 2017:

- MSCI World Index (EUR) +2.2%

- MSCI World Index (USD) +3.4%

- S&P 500 Index +8.2%

- European STOXX 600 Index +5.0%

- Japan Nikkei 225 Index +4.8%

- S&P Asia Pacific +11.9%

When you look at all the tables below what is unusual is that there was not even one strategy that performed really badly – worse was 0.5%.

The highest return was 20.5%.

What has worked so far in 2017?

Here is a short summary of what strategies worked best:

- World-wide - Qi Liquidity (low liquidity) +15.3%

- Europe - Price Index 12 months +19.2%

- North America - ERP5 +8.2%

- Japan - Price index 12 months +20.5%

- Oceania - Value Composite Two +15.2%

What did not work?

The following strategies performed badly:

- World-wide - Dividend yield +9.2%

- Europe - Dividend yield: +12.6%

- North America - Price Index 12 months +0.9%

- Japan - FCF Score (stable and growing FCF) companies +13.0%

- Oceania - ERP5 +0.5%

(To get investment ideas using these strategies click here: Quant investing screener)

We improved the report – four regions

Since writing to you about the best performing strategies in 2016 (Your absolute best strategy in 2016) we have improved the report.

This means you can now see the best investment strategies as follows:

- For all markets

- European markets

- North American markets

- Japanese Markets

- Other Asian and Oceanic markets

This gives you a much better idea of why your portfolio out- or under-performed and what strategies worked in the markets you invest in.

Before I show you the exact strategies and their returns first some information on what we tested and how we calculated the returns.

How we tested the 19 investment strategies

We looked at the performance of the following 19 investment strategies over the six month period from 1 January 2017 to 30 June 2017:

- Large vs small companies

- Book to Market value (inverse of price to book)

- Earnings yield (EBIT / EV)

- Qi Value rank

- Price Index 6m (Current share price / Share price 6 months ago)

- Price Index 12m (Current share price / Share price 12 months ago)

- Value Composite One rank (VC One)

- Value Composite Two rank (VC Two)

- ERP5 rank (Ranking based on Price to Book, Earnings Yield, Return on invested capital (ROIC), 5 year average ROIC)

- Shareholders Yield (Dividend yield + Percentage of Shares Repurchased)

- Dividend Yield

- Dividend growth 5 years (The geometric average dividend per share growth rate over the past 5 years)

- Magic Formula rank (MF Rank) (developed by Joel Greenblatt)

- Piotroski F-Score

- Qi Liquidity rank (Adjusted Profits / Yearly trading value)

- Gross Margin Novy Marx (gross profits / total assets)

- Free Cash Flow (FCF) Score (Calculated by combining Free cash flow growth with free cash flow stability)

- Adjusted Slope avg (125d, 250d) (This indicator is the annualized exponential regression slope, over the past 125 and 250 trading days, multiplied by the coefficient of determination (R2)

- Adjusted Slope (90d) (This is the annualized exponential regression slope multiplied by the coefficient of determination (R2) over the past 90 trading days)

7,000 companies worth more than $50 million

We excluded companies with a market value less than $50 million, to make sure that we only look at companies you can buy and sell easily.

Markets worldwide

We included markets worldwide because only when you look at markets worldwide can find the best companies that fit your investment strategy.

The following stock markets were included:

- USA

- Canada

- Eurozone countries

- United Kingdom

- Switzerland

- Norway

- Denmark

- Sweden

- Australia

- New Zealand

- Hong Kong

- Singapore

This gave us a list of about 7,000 companies.

(To take your investing to the next level click here: Quant investing screener)

Returns in home currency

The returns were calculated on the exchange in the country where the company is registered and we included dividends.

No adjustments were made for currency movements.

All companies in five groups – Quintile 1 the best

For each of the strategies on 1 January 2017 we divided all the companies into five groups (20%) or quintiles.

Quintile 1 shows the companies that scored best for all the strategies we tested - Quintile 5 the worse.

For example, Quintile 1 shows the return of the 20% of companies with the highest book to market ratio (lowest price to book) at the start of the year. And Quintile 5 shows the return of companies with the lowest book to market ratio (highest price to book ratio).

For Price Index 6m quintile 1 show companies with the best momentum (biggest share price increase over 6 months) and quintile 5 companies with the biggest price fall in the previous 6 months.

For Piotroski (F-Score) quintile 1 shows the return of companies with the best Piotroski F-Score (9 or 8) and quintile 5 those with the worse F-Score.

For the Size strategy quintile 1 shows the return of the 20% of companies with the biggest market value and quintile 5 the 20% smallest companies.

The tables are colour coded

All tables are colour coded with the best performing strategies shown with a green background and the worse performing strategies with a red background.

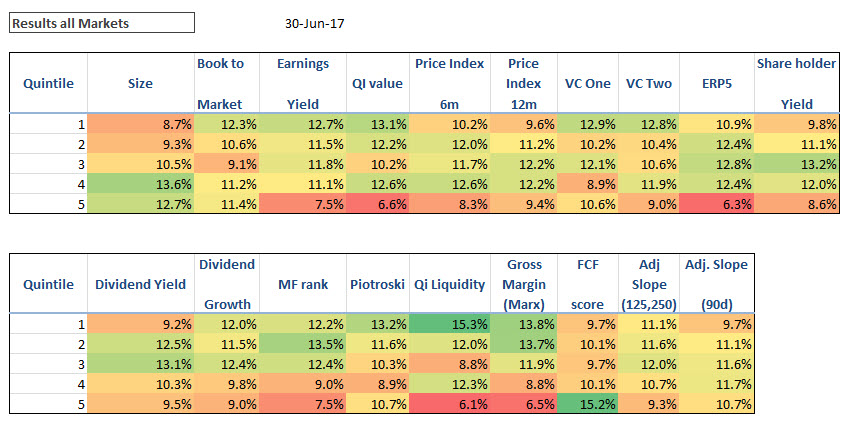

What worked world-wide?

The following table summarises how all 19 investment strategies performed world-wide:

Best performing strategies worldwide Source: www.quant-investing.com

Click image to enlarge

How all the best rated companies (Quintile 1) performed:

- Average return Quintile 1 of all strategies: 11.5%

- Maximum return of Quintile 1 strategies: 15.3%

- Minimum return of Quintile 1 strategies: 8.7%

What worked?

Here are the two best performing strategies:

- Low Liquidity (Adjusted Profits / Yearly trading value) companies +15.3%

- Good Piotroski F-Score companies +13.2%

What did not work?

These strategies did not do as well (still good returns).

- High dividend yield +9.2%

- Price Index 12m (momentum) +9.6%

- Large companies (not really a strategy) +8.7%

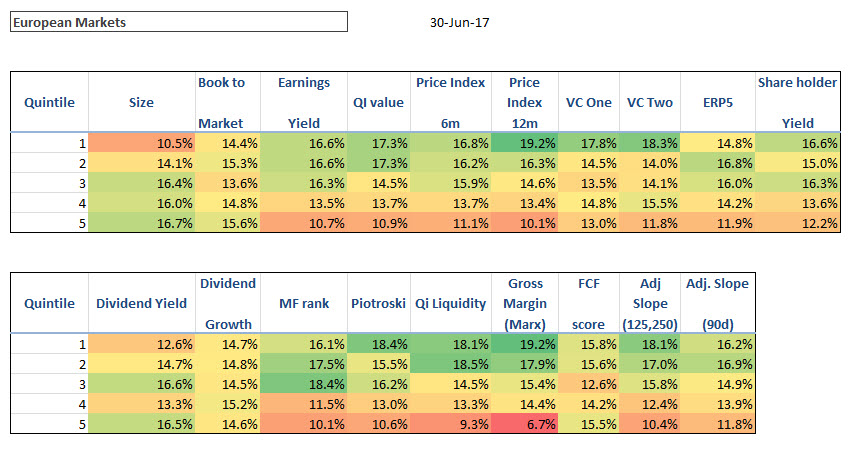

What worked in Europe?

Below is the performance of all 19 strategies in Europe:

Best performing strategies in Europe Source: www.quant-investing.com

Click image to enlarge

How all the best rated companies (Quintile 1) performed:

- Average return Quintile 1 of all strategies: 16.4%

- Maximum return of Quintile 1 strategies: 19.2%

- Minimum return of Quintile 1 strategies: 10.5%

What worked?

These were the best two strategies:

- Price Index 12 months (12m momentum) +19.2%

- Gross Margin Novy Marx (gross profits / total assets) 19.2%

What did not work?

The two worse performing strategies were:

- Large companies (not really a strategy): 10.5%

- Dividend yield: 12.6%

- Book to Market: 14.4%

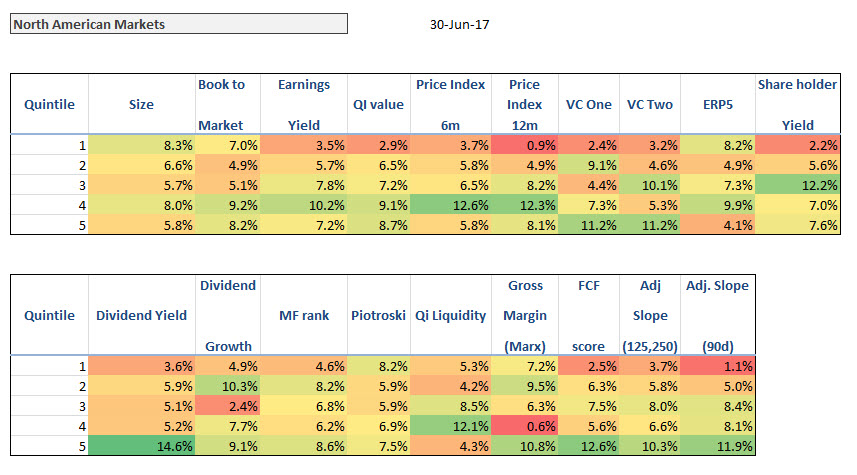

What worked in North America?

Below is the performance of all 19 strategies in North America:

Best performing strategies in North America Source: www.quant-investing.com

Click image to enlarge

How all the best rated companies (Quintile 1) performed:

- Average return Quintile 1 of all strategies: 4.4%

- Maximum return of Quintile 1 strategies: 8.3%

- Minimum return of Quintile 1 strategies: 0.91%

What worked?

The two best performing strategies were:

- Large companies +8.3% (not really a strategy - perhaps due to large tech companies)

- ERP5 +8.2%

- Piotroski F-Score +8.2%

What did not work?

The two worse performing strategies were:

- Price Index 12 months +0.9%

- Adjusted slope 90 days +1.1%

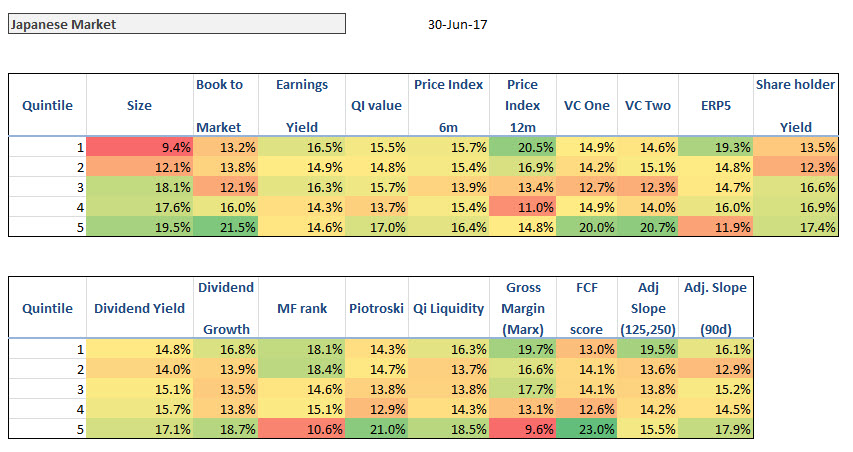

This was your best strategy in Japan

Best performing strategies in Japan Source: www.quant-investing.com

Click image to enlarge

How all the best rated companies (Quintile 1) performed:

- Average return Quintile 1 of all strategies: 15.9%

- Maximum return of Quintile 1 strategies: 20.5%

- Minimum return of Quintile 1 strategies: 9.4%

What worked?

- The two best performing strategies were:

- Price index 12 months +20.5%

- Gross Margin Novy Marx (gross profits / total assets) +19.7%

What did not work?

The two worse performing strategies were:

- Large companies (not really a strategy) +9.4%

- Good FCF Score (stable and growing FCF) companies +13.0%

- Book to Market +13.2%

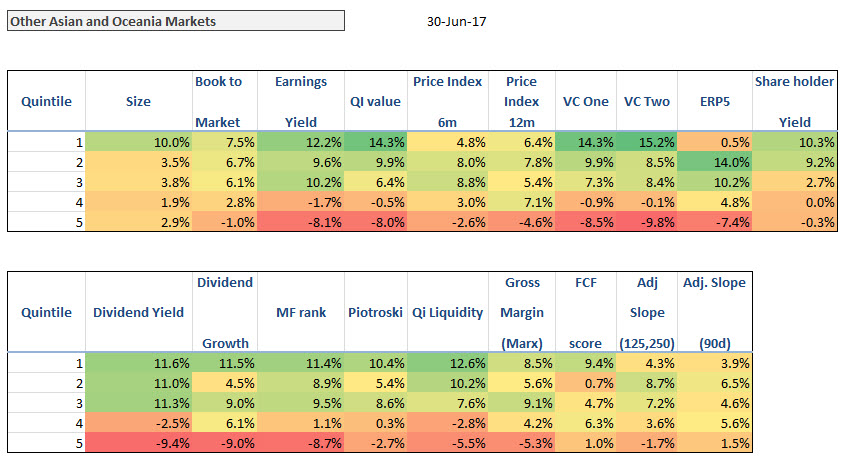

What worked in Asia and Oceania Markets?

(Australia, New Zealand, Hong Kong and Singapore companies are included in this analysis)

Best performing strategies in Asia and Oceania Source: www.quant-investing.com

Click image to enlarge

How all the best rated companies (Quintile 1) performed:

- Average return Quintile 1 of all strategies: 9.4%

- Maximum return of Quintile 1 strategies: 15.2%

- Minimum return of Quintile 1 strategies: 0.5%

What worked?

The two best performing strategies were:

- Value Composite Two +15.2%

- Qi Value +14.3%

What did not work?

The two worse performing strategies were:

- ERP5 +0.5%

- Adjusted slope average 125 and 250 days +4.3%

Returns all over the place – is normal

As I mentioned in the introduction the best performing strategies were all over the place, but as you know over a 6 month period anything is possible in the markets.

Like you I also find it interesting to see what has worked and what hasn’t, even if it is just to understand why my portfolio did well or why not.

A quick warning

Please remember just because a strategy did well so far this year does not mean it will continue to do so. As you can see the exact same strategy was the best in one region and also the worse in another region.

Jumping on the best performing strategy so far this year will most likely be a bad idea, possibly a very bad idea.

In fact your best strategy for the rest of 2017 may be the worst performing strategy so far – this is not a recommendation.

Like you I also have no clue as to what strategy will work best in the future, and if someone says he does, he is lying.

To find your best investment strategy take a look at this article: How to find your best investment strategy – not the one you expect

If you want to see details of all the very best strategies we have tested click here: Best investment strategies we have tested

PS To get this report on a daily basis (you can pay more for an inexpensive lunch for two) as well as the tools to implement all 19 strategies in your portfolio sign up here.

PPS It’s so easy to put things off, why not sign up right now?