The newsletter turned 12 and no one noticed

When completing the half year report earlier this year I noticed that we have been publishing the newsletter for more than 12 years.

The first newsletter was sent out on 19 July 2010, about one and a half years after the March 2009 low after the financial crisis.

Great timing?

Great timing you may be thinking?

We didn't time it that way of course we had no way of knowing that the market turned around in March 2009 but in hindsight it was good. The thing is no one knew that at the time.

You can clearly see how uncertain thing were at the time as this is what we wrote about the first two companies we recommended:

"In spite of these very acceptable financial results the share prices have not moved up much from the lows reached in March 2009, giving you the ideal opportunity to invest.

I have already bought both companies for my own portfolio as I found them so attractively priced.

Quite frankly, I would understand if you are hesitant to invest, especially in companies based in Europe which is currently in the grip of a recession and a sovereign debt crisis.

But it is exactly in tough times like these when you inevitably find the biggest bargains, as companies are avoided and overlooked by investors.

My experience has been that as long as a company is on a sound financial footing and attractively priced it is a mistake not to invest."

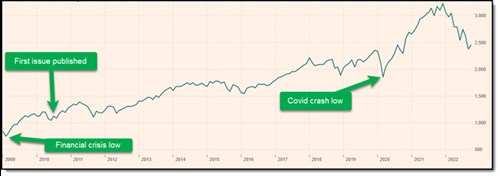

What the journey looked like so far

This is what the journey looked like so far.

Source: MSCI World Price Index USD

As you can see it has not been plain sailing, lots of ups and downs to get where we are at the moment.

Continues improvement

We knew that we would be facing tough times. That is why we continued to test the newsletter’s as well as other investment strategies. To improve all the time.

We also improved risk management. In March 2015 we implemented a strict 20% trailing stop loss strategy.

This was to sell losing investments fast and let winners run.

Stop buying when markets are falling

After a lot of thinking and research we realised we had to find a way to lower losses when markets start falling. You know when markets fall, they start falling together – in more technical terms – they become correlated.

This means, when markets are falling, and you keep on buying, the companies will soon be sold because the trailing stop loss will be triggered.

So, in spite of you buying companies that meet your investments strategy you will be selling just because the market overall is falling.

This is definitely not what we want!

So, in December 2017 we implemented a rule that says - No new investments when markets are falling. In practical terms this means no new companies are recommended if a market is trading below its 200-day simple moving average.

Make the most of market crashes

When the markets crashed as the Corona pandemic hit, we were worried, but we also realised that it was a great investment opportunity as investors were selling everything all at once just to get out.

We did not want to bet the house (invest heavily), but we wanted to selectively recommend very high-quality companies that had a good chance to survive and do well when things returned to normal.

This is how in April 2020 the Market Crash portfolio was born.

You can read more about the exact criteria of the strategy here: Quant Value Crash portfolio started

Basically, the difference between the "normal" recommendations and Market Crash portfolio is that the Crash Portfolio recommends ideas in spite of falling markets (being below their 200-day simple moving average).

And the crash portfolio uses a LOT stricter quality ratios and does not look at momentum (remember markets are falling so momentum is bad everywhere) when looking for ideas.

PS Not a newsletter subscriber yet? Sign up while the ideas are still fresh, it costs less than an lunch for two, click here to: Get the Quant Value newsletter now

PPS It is so easy to put things off, why not sign up right now before you forget