This is the editorial of our monthly Quant Value Investment Newsletter published on 2024-03-05. Sign up here to get it in your inbox the first Tuesday of every month.

More information about the newsletter can be found here: This is how we select ideas for the Quant Value investment newsletter

This month you can read my answers to a few questions by subscribers:

- Do world regions have different returns with the same strategy

- Why no recommendations in a North America?

- What about company sanctions?

But first the portfolio updates.

Portfolio Changes

Europe – Buy Two

Two new recommendations this month as the index is above its 200-day simple moving average.

The first is a ridiculously undervalued Norwegian container shipping company trading at Price to Earnings ratio of 1.5, Price to Free Cash Flow of 2.3, EV to EBIT of 1.6, EV to Free Cash Flow of 2.6, Price to Book of 0.7 with a dividend yield of 44.3%.

The second is a growing, debt free, UK specialist staffing company trading at Price to Earnings ratio of 9.9, Price to Free Cash Flow of 7.5, EV to EBIT of 6.1, EV to Free Cash Flow of 6.8, Price to Book of 2.5 and it currently pays a dividend of 3.7%.

North America – Buy One

One new recommendation this month as the index is above its 200-day simple moving average.

The company is engaged in the design, manufacture, sales and service of magnetic resonance imaging (MRI) scanners. It is debt free and trading at Price to Earnings ratio of 13.4, Price to Free Cash Flow of 13.4, EV to EBIT of 7.6, EV to Free Cash Flow of 12.0, and Price to Book of 0.9.

Asia – Buy Two – Sell One

Two Japanese recommendations this month as the index is well above its 200-day simple moving average.

The first is a Japan-based seller of electrical equipment and supplies trading at Price to Earnings ratio of 7.0, Price to Free Cash Flow of 8.6, EV to EBIT of 1.2, EV to Free Cash Flow of 2.0, Price to Book of 0.7. It has a lot of cash (54% of book value), and it pays a 2.4% dividend of that is growing fast.

The second is a Japan-based is a geospatial information service company. It is currently trading at Price to Earnings ratio of 8.4, Price to Free Cash Flow of 5.0, EV to EBIT of 5.1, EV to Free Cash Flow of 4.4, Price to Book of 1.0 with a growing 3.6% dividend yield.

Sell One

Sell SK-Electronics CO., LTD. at a profit of +112.5% as it no longer meets the portfolio’s selection criteria.

Crash Portfolio – Nothing to do

No new Crash Portfolio ideas as most markets have recovered.

To date the 15 Crash Portfolio ideas, recommended between August 2022 and May 2023, are up an average of 30.6%!

Subscriber Questions & Answers

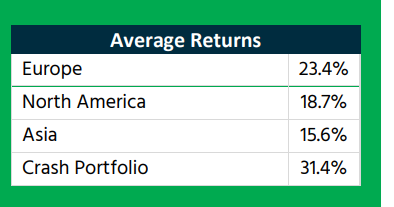

Question #1 – Average returns

How do we calculate the Average Returns on the first page of the newsletter?

In other words, these returns:

Answer:

The average return refers to the overall average return of all the companies recommended in those specific regions since the start of the newsletter.

This figure is not restricted to a particular year or the current portfolio but includes all recommendations to give a broad view of the performance over time.

I added an explanation below the table this month.

Question #2 – Do regions behave differently?

The newsletter makes recommendation in North America, Europe and Asia using the same investment strategy. I assume different market behave differently because of cultural, economic and investor mentality.

Have you ever analysed if a different investment strategy may work better in different regions?

Answer:

It may be that that markets can behave differently based on several factors such as culture, investor behaviour, and economic conditions.

Even if this is so I have not seen any research on this and I know of no way to capture this. Even the same investment strategy performs differently in the same region over time, sometimes it works other times not.

For example, the US market has seen periods of outperformance, making it relatively expensive. The newsletter’s focus however always stays the same; finding high-quality undervalued momentum companies wherever they may be.

Now these are mainly in Asia. It is however important to note that this shift reflects the market dynamics and not a bias towards any region.

Question #3 – Why no recommendations in a North America?

In the February newsletter you made no recommendations in North America even though the S&P 500 was above its 200-day simple moving average.

Why is this? Is it because no company passes the "check list test" or some other reason?

Do you give yourself some place of free choice that is not as strict as mere what the system says, and the checklist approved? Does your opinion also play a role?

Answer:

When it comes to recommendations, our primary aim is to find the most undervalued quality momentum companies available.

The absence of recommendations in a specific region, like the US currently, is due to the comparative analysis of available opportunities. If a region is expensive, we find that companies from other areas more attractive based on our criteria.

The newsletter’s investment system is to minimize human bias and rely on the data to guide our selections. However, we do consider industry diversification to avoid overconcentration in any single sector. For instance, despite finding many undervalued shipping companies now, we aim to keep a balanced portfolio by not over-representing any single industry.

Question #4 What about company sanctions

A subscriber tried to buy the Chinese company using his European broker (which uses a US custodian bank). They said he cannot buy the company as it is in the US sanction list.

He was not sure if his broker was wrong and was also unsure, if he wanted to invest in companies that are on sanctions lists. Or at least not without mentioning it in the write up you give each recommendation.

Answer:

With the newsletter we do not want to get involved with politics, Environmental, Social, and Governance (ESG) or moral issues.

We simply want to give you the best ideas we can find that fits the newsletter's investment strategy.

These issues are out of our hands and with subscribers throughout the world what issues affecting who should we consider? As you can see it quickly becomes complex.

We simply want to give you the best investment ideas we can find and leave it up to you to decide what you want to buy.

Reading recommendations

Brian Chingono's insightful article, "Rule, Britannia!" looks at the hidden investment opportunities in the UK's post-Brexit economy, particularly for small companies.

His analysis comparing UK and European corporate earnings, uncovers surprising shifts in profit margins and valuations.

Is the UK market's downturn an overreaction, or are there excellent opportunities for investors?

Most Important Point:

Post-Brexit, UK small-cap companies now trade at a significant discount compared to their European counterparts, despite historically higher profit margins. This change presents potential investment opportunities, particularly for private equity firms using the UK's discounted valuations.

In the interesting article "Magnificently Concentrated: Your Active Managers are More Competent Than They Look" Ben Inker and John Pease from GMO talks about the unexpected edge of active managers amidst the S&P 500's increasing focus on a select few stocks.

They explore why the recent success of the index's top performers may not be the final word on investment strategy and that the era of active management might just be on the brink of resurgence.

Key Insight:

Despite the dominance of the top stocks in the S&P 500, active managers' strategic underweighting might soon pay off, challenging the notion of market efficiency and hinting at a brighter future for active management.

Your analyst wishing you profitable investing

P.S. The Quant Value newsletter is published on the first Tuesday of the month – so look for the next issue in your inbox on Tuesday 2 April 2024.

Not a subscriber? Click here to get ideas from the BEST strategies we have tested NOW!