This article shows you the back tests results of the ERP5 investment strategy and exactly how (step by step) to implement it in your portfolio.

A strategy to beat the Magic Formula

The ERP5 investment strategy was developed to when two friends set out to find a strategy to beat the Magic Formula developed by Joel Greenblatt.

How is the ERP5 ranking calculated?

The ERP5 investment strategy is a ranking system that uses the following four ratios.

- Earning Yield (EBIT / Enterprise Value) – Profits before interest and taxes compared to enterprise value.

- Return on Invested Capital (EBIT / (Net Working Capital + Net Fixed Assets)) – The return a company generates on the capital invested in the business.

- Price to Book (Market value / Book value) – share price compared to the book value of the company

- 5-year average Return on Invested Capital – Five year average EBIT to Five year average ((Net working capital) + Net Fixed Assets)

The name ERP5 comes from the first letter of the four ratios.

Best companies have the lowest ERP5 rank

To calculate the ERP5 ranking you rank each company against all the other companies based on each of the four ratios. Once you have ranked all the companies you add the individual rankings, for each ratio together, into one combined ranking for each company. You then rank all the companies by this combined ranking.

In the screener we group this combined ranking into percentiles (from 1 to 100); with 1 is the 1% of companies with the best ERP5 rank and 100 the worse ranked.

The ERP5 rank of more than 22,000 companies is available in the stock screener.

All calculations done for you

Don’t worry if this looks intimidating, the screener does all these calculations for you. You can find all the companies that fit this investment strategy with a few simple mouse clicks.

What returns does ERP5 generate?

Now we come to the most important question. Does the ERP5 investment strategy work?

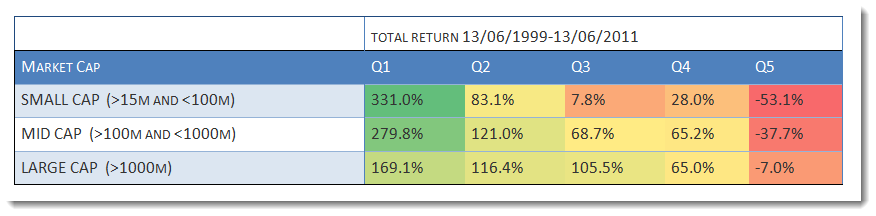

We tested ERP5 as an investment strategy in Europe over the 12 year period from June 1999 to June 2011.

Source: Quantitative Value Investing in Europe: What works for achieving alpha

As you can see companies with the lowest ERP5 values (the most undervalued companies), quintile 1 (Q1) in the above table, did a lot better than companies with a high ERP5 value, and did this for small, medium and large companies.

Substantially better than the market

Low value ERP5 companies all also substantially outperformed the market which returned only 30.54% over the same 12 year period.

This is how the above back test was done.

The back test universe and benchmark

The back test universe was a part of companies in the Datastream database containing an average of about 1500 companies in the 17 country Eurozone market during our 12-year test period (13 June 1999 to 13 June 2011).

We excluded banks, insurance companies, investment funds, certain holdings companies, and REITS.

We included bankrupt companies to avoid any survivor bias. For bankrupt companies, or companies that were taken over returns were calculated using the last stock market price available before the company was delisted.

We excluded companies with an average 30-day trading volume of less than €10 000.

It was not a good time to invest in stocks

The test period was most certainly not a good time to be invested in stocks.

The 12-year period included a stock market bubble (1999), two recessions (2001, 2008-2009) and two bear markets (2001-2003, 2007-2009).

Holding periods and quintile tests

Each year all the portfolios were formed on 16 June. We chose 16 June as most European companies have a December year-end and by this date all their previous year-end results would be available in the database.

The annual returns for our back test portfolios were calculated as the 12-month price change plus dividends received over the period. Returns were compounded on an annual basis.

This means each year the return of the portfolio (dividends included) would be reinvested in the strategy the following year.

The portfolios were all constructed on an equal-weighted basis.

In order to test the effectiveness of a strategy, we divided our back test universe into five equal groups (quintiles).

The 20% best ranked ERP5 of companies were put in the first quintile (Q1), the next in the second, and so on, with the 20 % of companies with the worst ERP5 ranking in the fifth quintile (Q5).

Click here to start using the ERP5 strategy in your portfolio NOW!

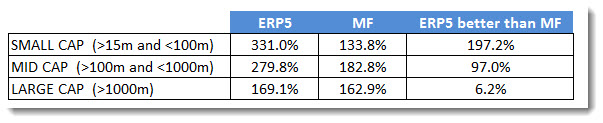

Does it beat the Magic Formula?

For the same 12 year period mentioned above we also tested the Magic Formula (applied to European companies), compared it to the ERP5 strategy and this is what we found:

The table shows the total 12 year return of both strategies with the last column showing by how much the ERP5 strategy beat the Magic Formula.

ERP5 did substantially better +200%

As you can see the ERP5 strategy, for all size companies, did substantially better than the Magic Formula, in fact for small companies if you would have had done nearly 200% better.

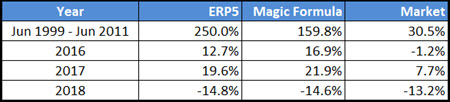

Recent results

Here are more recent results of the returns you could have earned if you invested in the top 20% ERP5 and Magic Formula companies world-wide in Europe.

As you can see the strategy continues to do well substantially beating the market!

In the past three years it performed only slightly worse than the Magic Formula. This is not unusual as all investment strategies have times where they do not perform as well.

But you can also improve the returns of the ERP5 strategy

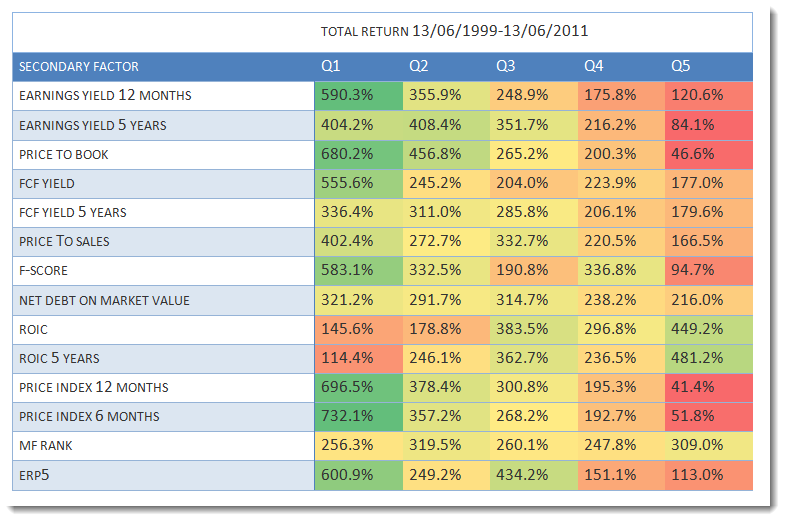

We also tested the ERP5 strategy with a lot of other ratios and as you can see in the table below the returns of the strategy can be substantially improved.

Source: Quantitative Value Investing in Europe: What works for achieving alpha

Look at column Q1

Look at the returns in column Q1. They show the returns generated by first selecting the 20% best ERP5 companies (most undervalued) and then sorting them by the items in the Secondary Factor column.

Best combination +732% was Momentum

This means you could have earned the highest return of 732.1% over 12 years if you invested in the best ranked ERP5 companies that also had the highest 6 month price index (price momentum).

Summary

As you can see the ERP5 investment strategy is something that deserves your serious attention because as a stand-alone strategy it has performed substantially better, not only than the market, but also better than the Magic Formula.

Click here to start using the ERP5 strategy in your portfolio NOW!

How to implement the ERP5 investment strategy in your portfolio

Because all the calculations are already done for you in the screener it is VERY easy to implement the ERP5 investment strategy in your portfolio.

The following is just an example; you can of course combine this strategy with any of the more than 110 ratios and indicators in the screener.

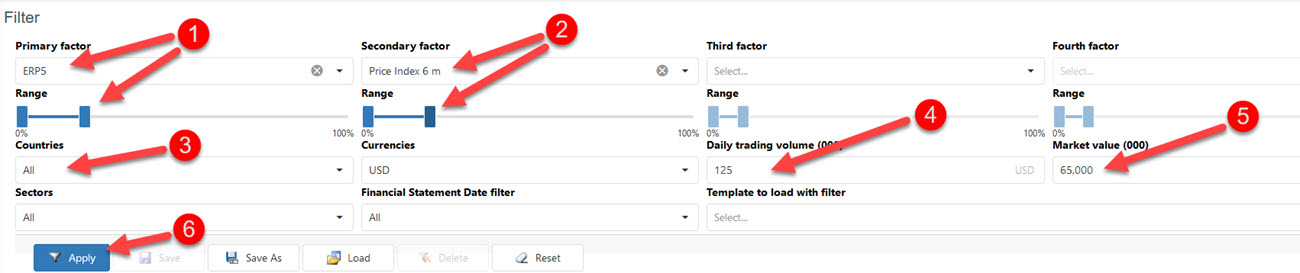

ERP5 momentum screen setup:

- As the Primary Factor or filter select the 20% of companies with highest ERP5 rank. To do this set the sliders from 0% to 20%.

- As a second factor select the 20% of companies with the highest Price Index 6m (six months price momentum). To do this set the sliders from 0% to 20%.

- Select the countries where you would like to invest by clicking on the drop down list below Countries.

- Set your Daily minimum trading volume - $125,000 in the image below.

- Select the minimum Market value of companies you would like to look for - $65m in the image below.

- Click on the Apply button to run your screen.

Click image to enlarge

In the results table click on the ERP5 Rank column heading once to sort the companies from low to high (the lower the ERP5 Rank the more undervalued the company is).

You now have a list of companies that fits the ERP5 momentum investment strategy.

Limit your losses

We strongly recommend that you use a strategy to keep your losses log. You can read more about that here: Truths about stop-losses that nobody wants to believe

Exact definition of all ratios – the glossary

You can see the exact definition of all the ratios and indicators in the Quant Investing Glossary

Further reading about the ERP5 investment strategy

You can read more about the ERP5 investment strategy in the following articles:

A better alternative to the Magic Formula?

Does systematic value investing really work? – Data driven back test

Wishing you profitable ERP5 investing

PS To find ERP5 investment ideas in the countries where you invest (for less than an inexpensive lunch for two) click here: Join today

PPS It is so easy to get distracted why not sign up today before it slips your mind?

Click here to start using the ERP5 strategy in your portfolio NOW!

Please note: This website is not associated with Joel Greenblatt and MagicFormulaInvesting.com in any way. Neither Mr Greenblatt nor MagicFormulaInvesting.com has endorsed this website's investment advice, strategy, or products. Investment recommendations on this website are not chosen by Mr. Greenblatt, nor are they based on Mr Greenblatt's proprietary investment model, and are not chosen by MagicFormulaInvesting.com. Magic Formula® is a registered trademark of MagicFormulaInvesting.com, which has no connection to this website.