We added 12 months minus 1 month (12-1 month) momentum to the Quant Investing stock screener.

How it is calculated

In the screener we call momentum Price Index and this is how it is calculated: Price Index 12m Minus 1m = Share price 1 month ago / Share price 12 months ago.

For example

Assume the current date is 1 October 2016.

Price Index 12m Minus 1m = Share price on 1 September 2016 / Share price on 1 October 2015.

The ratio shows you the return of a share price over the past year but excluding the last month.

This lets you screen out companies with a large jump in share price over the past month which studies have shown usually reverses shortly thereafter.

How to interpret results

A Price Index 12m Minus 1m value greater than 1 shows that there's been a price increase over the period whereas a value less than one shows that there has been a price decrease.

Click here to start using 12-1 month momentum in your portfolio Now!

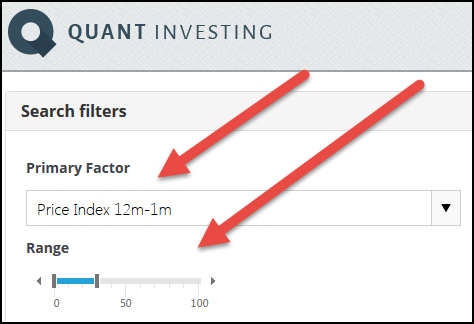

Available as a slider and output column

Twelve months minus one month momentum is available as a primary screening ratio which you can select using the slider, as well as an output column (so that you can see, filter and export the exact values).

This means you can select 12m minus 1m momentum and refine your search with the slider as shown below:

How to select the best companies

To see the 30% companies with the highest 12-1 month momentum set the slider from 0% to 30%.

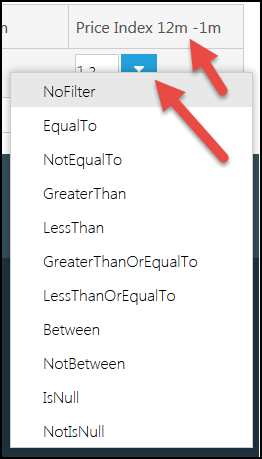

Select it as an output column

Or you can refine your search by sorting the values in the column (simply click the column heading) or by typing a value in the space below the heading and clicking the small funnel icon as shown in the screenshot below.

Click here to start using 12-1 month momentum in your portfolio Now!