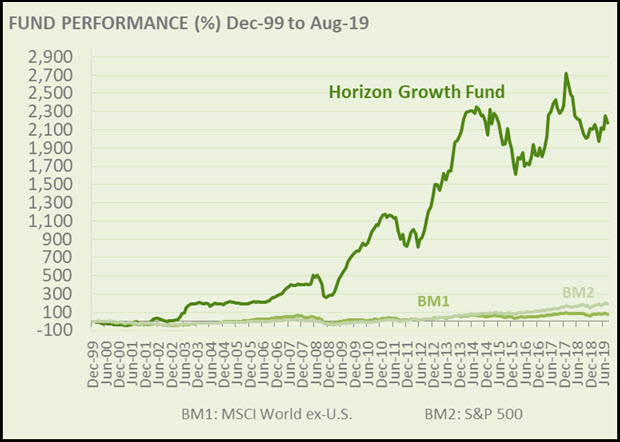

Would you have liked to earn 2176% over the past 19 years? I am sure you would and it is possible as John Tidd Kimball manager of the Horizon Growth Fund proved.

Here is more information on the fund’s performance:

Source: Horizon Growth Fund Quarterly Letter August 2019

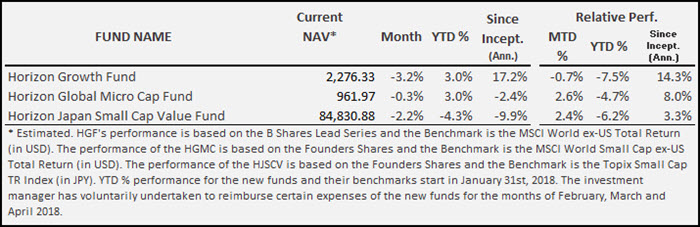

Source: Horizon Monthly Report August 2019

Yes, the last few years have not been easy (for all value investors) but the overall return has been outstanding.

After this interview the Horizon Growth Fund was closed. You can find information on John's follow up fund here: Hamco Global Value Fund.

About the Horizon growth fund

Here is some more information about Horizon.

They have an outstanding 19 year track record as bottom-up, deep value stock pickers that take big positions in their best ideas. The fund has a flexible mandate that allows them to invest in markets worldwide including hedging.

They currently have more than USD 130 million in total assets under management. Which includes a lot of their own money making them partners of their investors.

Click here to start finding your own Deep Value ideas NOW!

I also wanted to know more about John

I have been reading John’s fund letters for a few years and was often amazed at where in the world he finds interesting deep value investment ideas.

I wanted to know more about John and his investment approach and was really pleased when he agreed to the following interview.

Here is the interview

Describe your investment philosophy?

John Tidd Kimball:

We are Value Investors. It’s in our DNA.

We look for deep undervalued securities all around the world and we take investment decisions based on several factors such as long term growth potential, debt level, cash generation, liquidity, returns on equity and many others.

Our proprietary research process, independent mindset and confidence in our ideas have been key elements in our success during the last two decades.

How do you typically find ideas and what is your selection process before an idea gets added to the portfolio?

John Tidd Kimball:

As bottom up fundamental analysts, we start by screening the entire universe of active public equities and rank those with good ratios. The classic ones are Price to Book, Price Earnings, Price to Cash Flow, Net Debt to Equity, Return on Equity and many other.

Once we have interesting candidates we then go ahead and quickly analyze 10-20 years of the financial history, estimate our first approach of the intrinsic value and calculate the expected return. Throughout the years we have developed an internal template that allows us to focus in what really matters and get a quick idea on the potential of the company.

If we believe the investment is still interesting then we analyze in detail all the information we can get, not just from the financials and notes but from news, competitors, industry, general outlook of the economy, regulations that might impact, etc…

During this phase we also have a first contact with the company and usually try to speak with the Management team. This allows us to get a big picture of the business, ask some detailed questions to understand even better the financials and also to assess the quality of the management team.

Once we are convinced with the idea, we select those with good long term potential, low debt, good cash generation (and good usage of cash), good ROE and trading at low valuations.

What main indicators and ratios do you use in your selection process?

John Tidd Kimball:

We use the classic indicators such as the Price to Book, Price Earnings, Price to Cash Flow, Net Debt to Equity, Return on Equity and many others.

It’s also important how these ratios are combined with each other and the coherence between them.

The two most important are our expected return and risk level (net debt to equity).

How important is defining your investment universe correctly for investment success?

John Tidd Kimball:

We have a broad investment universe. We search for investment opportunities all around the world.

This is very important since it gives us the flexibility to go into markets with interesting valuations and sometimes not very well followed. This has allowed us to keep finding excellent companies at very good prices no matter the economic cycle of specific countries or regions.

What are your ideas concerning portfolio composition and the value of individual holdings in relation to the portfolio?

John Tidd Kimball:

We are more stock pickers than portfolio managers. We try to limit risk to specific sectors, countries etc. to have our risk diversified.

Click here to start finding your own Deep Value ideas NOW!

How do you size position size in your portfolio? (Equally weighed / Volatility weighted?)

John Tidd Kimball:

We don’t follow a special rule. It depends on the expected return and conviction.

We have had large position weights in the past with mixed results and now run trying to run a more balanced portfolio.

We don’t target volatility and I guess if we did it would be more volatility seeking. Probably one can make good returns from buying volatile investments.

Describe your biggest investing mistakes and what you've learned from them?

John Tidd Kimball:

I am always amazed at how many mistakes we make and still have a pretty decent track record.

Just to give a specific example, we learned the hard way about the regulatory and political risk associated with financial investments during a crisis, especially with banks. These entities with highly leveraged balance sheets can turn out to be good investments but also can get you killed and destroy shareholders value by issuing shares in the worst possible moment.

How concentrated is your portfolio? Do you follow any key risk-management guidelines in managing your portfolio?

John Tidd Kimball:

The general guidelines is that whenever we find a company with good potential and an interesting risk-adjusted return, we are not afraid of concentrating the portfolio.

However, our concept of concentrating has change a bit during the last two decades mainly because of the size of our fund and the liquidity risk it entails.

For the Japan and Micro cap funds we run a more diversified portfolio since we try to manage those with a more automatic screening and selection process.

We are also about to start advising a new UCITS Fund in Spain which will also have a diversified portfolio allowing a daily liquidity NAV and a reduced risk profile.

What is your view on the use of stop-loss strategies?

John Tidd Kimball:

We don’t use stop-loss strategies and don’t recommend it.

If the price goes down and nothing has changed on our investment idea it is very likely we will increase our position. And if nothing has changed and a position has gone down substantially we need to be buying more.

What do you think of short selling?

John Tidd Kimball:

We don’t do short selling either.

We try to focus our brains in what we are good, and that’s finding long investment ideas. We have index hedges in recent years and it’s been a sizeable distraction and to date a drag on performance.

Hopefully the divergence between stock and bond prices will be resolved very soon.

What is your 80/20 investment strategy or principle? (The most important 20% you must do to get 80% of the highest investment returns)

John Tidd Kimball:

Pick good investments.

Don’t panic in a downturn and better yet when you see everyone else panicking have the confidence to be fully invested in equities.

Click here to start finding your own Deep Value ideas NOW!

How did your portfolio perform over the financial crisis?

John Tidd Kimball:

During the 2008 the portfolio declined 25% vs the MSCI World ex US Total Return (in USD) that decreased 44% and the S&P that fell 37%.

How did you manage the financial crisis or any large decline mentally?

John Tidd Kimball:

The financial crisis was a special case for us. We sensed something wasn’t very right at the moment and began accumulating cash a few years earlier.

When the downturn began, the cash protected our portfolio and the impact wasn’t extremely painful.

Moreover, it allowed us to invest the necessary cash at very opportune prices. That’s the reason why we had such an outstanding post-crisis performance of 125% and 44% during 2009 and 2010, respectively.

One of the most mentally challenging crises was actually at inception.

Back in 2000, when we began managing the Horizon Growth Fund, we were investing in south Asian countries.

During the Asian Financial crisis, equity prices were on the floor and so was the currency. Many interesting opportunities were found. However, during the year, prices kept falling and our first year we had a performance of -38%.

Despite this, we never thought about quitting. We were convinced in the value investing philosophy and that the equities we selected were good investments in the long run.

And so it did.

The next year we had a small double digit gain but the following two years were very good, with +52% and +174%, during 2002 and 2003, respectively. The key is picking good investments and having confidence in what you are doing.

If you were a private investor with about €50,000 to €100,000 to invest how would you go about it?

John Tidd Kimball:

It depends on many factors such as the return objectives, risk profiles and constraints (including taxes), but given that I’m a long term investor, I would have a portfolio or fund that definitely includes equities on it.

Nowadays it’s the only type of investment I see with interesting long term returns.

Anything else you would like to mention?

John Tidd Kimball:

Investing is a fascinating and stimulating activity. At Horizon we have a constant drive to improve our skills and abilities and that makes this all very interesting.

John, thanks for your time

PS Are you looking to a stock screener to implement a deep value investment strategy worldwide? You can sign up right here

PPS It costs less than an inexpensive lunch for two each month and if you don’t like it you get your money back. Sounds fair? Why don’t you sign up right now?