Have you ever wondered how much you should invest in each stock? This post explains why simple equal-weighting is not the best approach and how risk-based position sizing—called risk parity—can improve your portfolio's stability and returns. You will learn:

- Why position sizing is really about risk allocation, not just money allocation.

- How investing the same amount in volatile and stable stocks increases your portfolio’s risk.

- How risk parity (Target Weight) helps you adjust your investment size based on stock volatility.

- How to use the Quant Investing stock screener to find Target Weights for your portfolio.

By the end, you will have a practical strategy to optimise your portfolio for more consistent performance.

Estimated Reading Time: 6 minutes

Have you ever thought of how much you should invest in each stock in your portfolio – also called position sizing?

You can simply diversify your portfolio over 15 to 30 companies. To do this you divide the total amount you want to invest by that number and invest the same amount in each company.

But this approach has a problem…

You Are Not Allocating Money You Are Allocating Risk

Think about it, with position sizing, you are not allocating money, you are allocating risk between the stocks in your portfolio.

Should you invest the same amount in a volatile (big up and down movements) stock as in a company with a stable share price?

Probably not.

Think of an investment in Nestle compared to very undervalued small cap company with problems.

The Same Investment Gives You More Risk

If you invest the same amount in each company you increase the risk in your portfolio to the most volatile companies.

For example, some stocks in your portfolio may move up and down by 0.3% per day while other companies may move up and down by over 3%. This means the profits (or losses) of your portfolio depends on the more volatile companies.

To give more stable companies a chance to give you the same return you should invest a bigger amount in them.

It Is Called Risk Parity

This idea is called risk parity – it means the position size of an investment is based on the volatility of the company’s stock price.

We Call It Target Weight

In the Quant Investing stock screener we call risk parity position sizing Target Weight and it is simply the volatility adjusted recommended position size (in %) for a stock in your portfolio.

This is what it looks like:

Suggested position size (Target Weight) based on the stock’s volatility

How is Target Weight calculated?

Don’t worry about the calculations below - I included it here to show you exactly how risk parity works and how it is calculated.

In the Quant Investing stock screener this is all done for you, keep reading and I will show you:

- Where to find it

- How to use it in your portfolio.

To start using Target Weight in your portfolio now - Click here

Risk Parity Formula:

This is how risk parity is calculated.

Number of shares to buy = (Total capital you have to invest * Risk Factor) / ATR

Total capital you have to invest = Is the total amount you want to invest in the stock market, for example $100,000.

Risk Factor - We use 0.1%

Risk factor is an arbitrary number that you choose to determine the daily impact - percentage movement - of a stock in your portfolio.

For example, if you choose 0.003, then you are setting the daily movement impact of this stock on your portfolio of 0.3%. This of course assumes that the Average True Range (ATR) (explained below) stays more or less the same as in the recent past.

The lower you set the Risk Factor, the smaller your investment in the stock will be. In the screener to calculate the target weight we use a risk factor of 0.001 or 0.1%

Average True Range - ATR - We use the past 20 trading days

Average True Range (ATR) is the average volatility of the company’s stock price measure as the maximum of the days move (high or low) compared to the previous day.

ATR is shown in the value of the stock’s price movements, for example $1.3 or €0.4.

In the screener we use the past 20 trading days (past month) to calculate the average True Range (ATR).

Target Weight Example

Here is an example so you can see how Target Weight is calculated in the screener:

- Total capital you have to invest: €100,000

- Risk Factor: 0.001 (equals 0.1%)

- ATR of the stock: €1.10

- Current share price: €43.50

The number of shares you should buy is: (100,000 x 0.001)/1.10 = 91 shares

Value of the transaction = 91 shares x €43.50 = €3,959 or 3.96% (3,959/100,000) of your portfolio

Maximum Position Size of 7%

In the screener the position size or Target Weight varies from 0% to 7%.

We have limited the maximum position size to 7% or 15 positions.

We chose this number because 15 companies give you most of the benefits of diversification. This large position size of course only applies to the companies with the lowest volatility.

Please remember that the Target Weight is only a suggestion, you are free to use whatever weighting you feel comfortable in your portfolio.

To start using Target Weight in your portfolio now - Click here

But Doesn’t It Changes All the Time?

But the volatility of a stock changes all the time, you may be thinking.

That is correct and that is why the Target Weight changes on a daily basis. This however does not mean that you must change your position size all the time - that will cost too much in trading fees.

To keep trading costs low we suggest that you check your position size on a monthly basis and only trade if the Target weight has changed by more than a certain percent that you can set yourself, a change of 2% or more, for example.

This means if the Target Weight was 5% when you invested you will only adjust your investment in the stock if the Target Weight changes by more than 2%, to 3% for example. If this happens you sell until the company makes up only 3% of your portfolio.

If a stock price has a large movement in a day, for example more than 10% you may want to adjust your investment immediately as this move signals that something important has happened which makes an adjustment necessary.

Where Can You Find It?

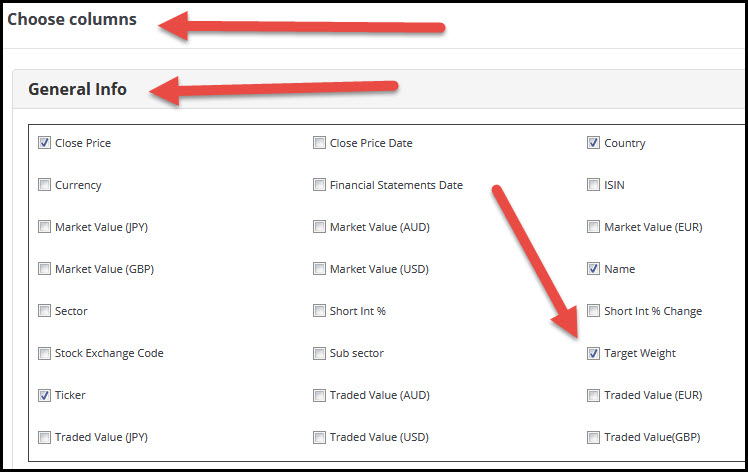

In the stock screener the Target weight is available for more than 22,000 companies.

To see the Target Weight simply select it as an output column of your screen.

Click image to enlarge

How to select Target Weight as an output column

How To Keep Track of The Target Weight for Your Whole Portfolio?

As mentioned the Target Weight changes on a daily basis. To keep track of it (and all the other ratios for your portfolio) simply save watchlist of all the companies you want to track.

This is how you do it.

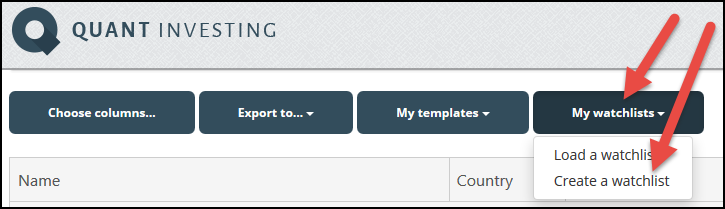

Create your watch lists

Watch lists are very easy to create.

Once you have logged into the screener click the My Watchlists button. Then click Create a Watchlist.

How to create a watchlist

Type in the name of the watch list you want to create and click the Save button.

How to save a watchlist

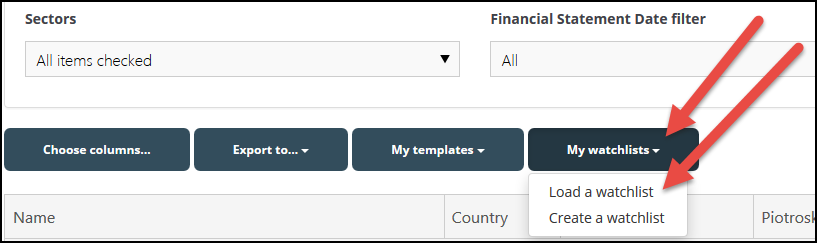

Add companies to your watch list

To add companies you first have to load your watch list. To do this click the My watchlists button then click Load a watchlist.

First you load your watchlist

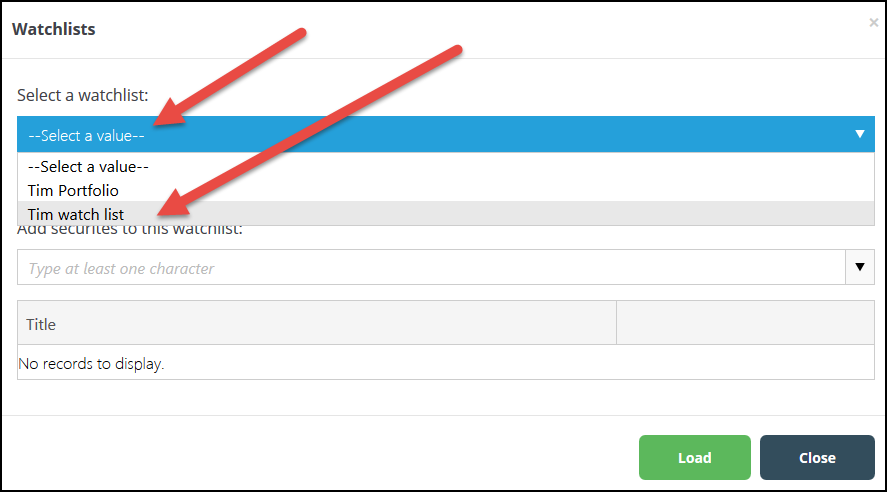

Load a watch list by clicking the drop down list below the heading Select a watchlist, and then click on the watch list you want to add companies to.

How to select a watchlist

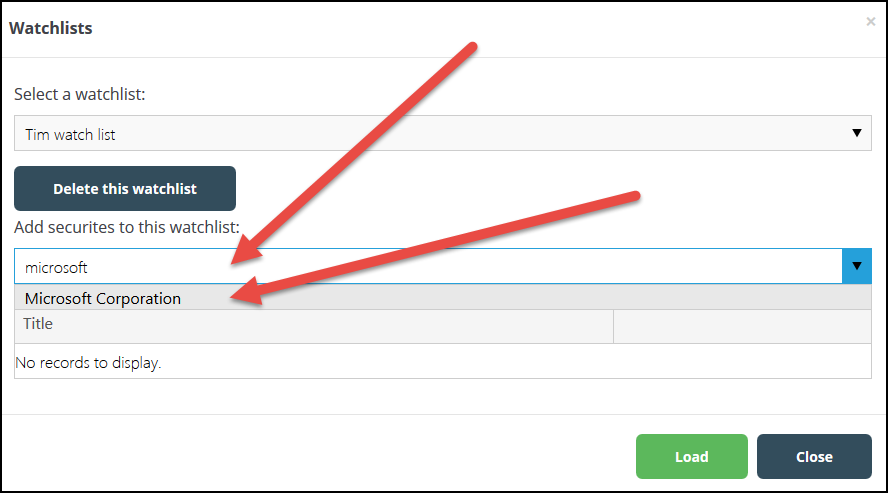

Once the watch list is loaded you can add companies by typing the name of the company in the block below the heading Add securities to the watch list.

As you type a list of company names will appear. To add the company simply click on the company name.

How to add a company to the watchlist

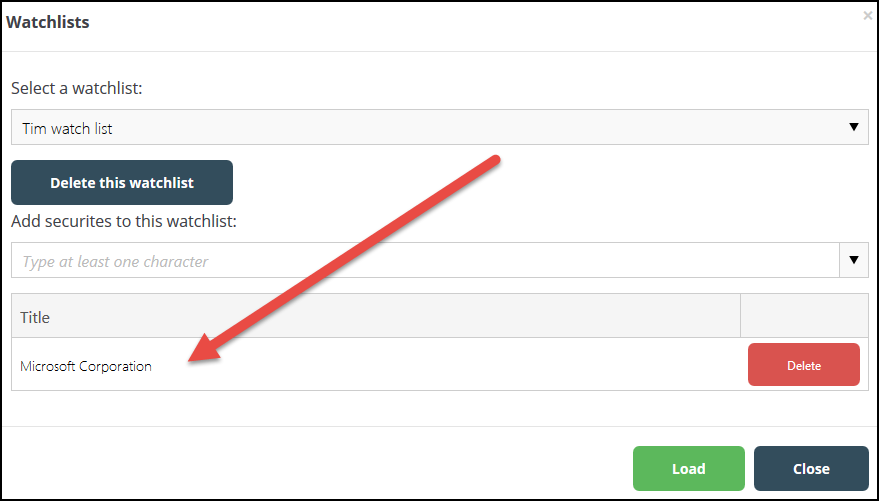

When you have added a company it will appear in the list below the search field.

Company successfully added to the watchlist

Frequently Asked Questions Position Sizing and Target Weight

1. Why should I care about position sizing?

Position sizing is not just about dividing your money equally among stocks. It is about managing risk. If you invest the same amount in a stable stock like Nestlé and a volatile small-cap stock, your portfolio will be too dependent on the riskier stock. Proper position sizing helps balance your portfolio for better long-term returns.

2. How does risk parity (Target Weight) help me?

Risk parity adjusts your investment size based on a stock’s volatility. If a stock moves a lot, you invest less in it. If it moves less, you invest more. This way, no single stock dominates your portfolio’s ups and downs.

3. How is Target Weight calculated?

Target Weight is based on the volatility (ATR) of a stock. The formula is: Number of shares to buy=(Total capital×Risk Factor)/ATR

Do not worry about the calculations—the Quant Investing stock screener calculates this for you.

4. Does this mean I have to rebalance my portfolio every day?

No. Stock volatility changes daily, but adjusting your positions too often will increase trading costs. Instead, check your portfolio once a month and only rebalance if a stock's Target Weight changes by more than 2%.

5. What is the maximum position size I should have?

The maximum recommended position size is 7%. This ensures you stay well-diversified while still benefiting from strong stocks. This limit applies to the least volatile stocks.

6. Where can I find the Target Weight for my stocks?

In the Quant Investing stock screener, you can add Target Weight as a column in your stock screen. It is available for over 22,000 companies worldwide.

7. How do I track Target Weight for my whole portfolio?

Create a watchlist in the stock screener. This allows you to see all your stocks' Target Weights in one place and monitor changes easily.

PS To get access to Target Weight position sizing on all the more than 22,000 companies included in the screener click here: Sign me up!

A subscription costs slightly more than €1 per day and has more than 110 ratios and indicators you can use to look for investment ideas.

PPS Why not sign up right now while it's still fresh in your mind?

To start using Target Weight in your portfolio now - Click here