If you found this article you have most likely read about dual momentum, the investment strategy described in the very interesting book by Gary Antonacci called Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk.

About Gary Antonacci

Gary Antonacci is an interesting guy and has been around investing for a long time.

Gary has a Harvard MBA and over 35 years of experience researching, developing, and using investment strategies that have their basis in academic research. This is similar to what we also here at Quant Investing.

Gary is an expert on the practical applications of momentum investing. His research on momentum won first place in 2012 and second place in 2011 of the prestigious Wagner Awards for Advances in Active Investment Management. These awards are given annually by the National Association of Active Investment Managers.

You can read more about Gary on his website called Optimal Momentum.

The idea behind momentum

Momentum is based on the idea that a body in motion tends to stay in motion.

In terms of investing momentum it means the movement of a company’s stock price which can be either up (positive momentum) or down (negative momentum).

We like momentum

If you have read the research report Quantitative Value Investing in Europe: What Works for Achieving Alpha you know that (contrary to what we believed) we discovered that momentum works. In fact it formed part of all the best investment strategies we tested.

You can read more about all the best investment strategies we tested here: Quant-Investing best investment strategies.

We found relative momentum works

The type of momentum we found that works is called relative momentum. To calculate it you compare the movement of one company’s share price to the share price movements of other companies.

Buying the most undervalued companies with the best relative momentum gives you market beating returns but it does not help you to reduce volatility (large up or down share price movements) or large falls in share prices.

What is absolute momentum?

Momentum, however, also works well on an absolute basis and it helps you reduce large losses.

To find a company’s absolute momentum, you compare the movement of its stock price with the return of a short term government bond (in the book Gary uses US Treasury bills) over a certain period.

If the stock price return minus the return of a short term government bond, called excess return, is greater than zero, then the company has positive absolute momentum.

Relative and absolute momentum differences

Gary explained absolute and relative momentum like this:

“Relative momentum looks at price strength with respect to other assets. It is like being on a train, then hopping on to a faster one that comes along.

Absolute momentum looks at an asset’s own positive excess return over a given time period. If the train you are on starts going backwards and there are no other trains moving in the right direction, you step off on to the platform.”

Dual momentum combines relative and absolute momentum

Dual momentum is the combination of relative and absolute momentum.

It is possible for a stock price to have positive relative momentum if it is strong relative to other companies and negative absolute momentum if its own trend has been down.

Similarly, it can also have positive absolute momentum if its trend has been positive (higher than short term bonds ) but negative relative momentum if another companies have gone up more.

Absolute momentum been neglected

In the book Gary makes an important point that researchers have thoroughly looked at relative momentum but that they have ignored absolute momentum until recently.

And this in spite of the fact that absolute momentum often provides better results and has more flexibility than relative momentum.

This was proven in a 2012 paper called Time Series Momentum by Tobias J. Moskowitz, Yao Hua Ooi and Lasse Heje Pedersen which showed that absolute momentum profits were very consistent across 58 different asset classes and markets.

12-months look back works best

In the paper they found a 12-month look-back period had the highest statistical significance (they tested look back periods from 1 to 48 months) when used with a one-month holding period.

In other words they looked at the return of 58 asset (commodity and bond futures, equity indices and currencies) over the past 12 months and if the return was greater than that of the US treasury bill rate they invested in the asset (went long) and if the return was negative they sold the asset short (went short).

They found that absolute momentum profits were positive for every one of the 58 assets they examined and that returns were largest when stock market returns were the most extreme (both up and down), which means absolute momentum can function as a hedge against extreme events.

Why use dual momentum?

In the book Gary says the best approach to investing is for you to use absolute and relative momentum together so that you use the advantages of both.

What look back period to use?

As the majority of academic literature covering both relative and absolute momentum agrees that a 12-month look-back period gives the best performance Gary also suggests that you also use a 12-month look-back period and apply it to both types of momentum.

How to use dual momentum

To do this you first use relative momentum to select the best-performing asset over the preceding 12 months.

You then apply absolute momentum as a trend-following filter by calculating if the excess return (the return of the asses minus the US Treasury bill return) over the preceding 12-months.

If it is positive, it means its trend is up, and you invest in the asset. If the asset’s excess return over the past year is negative, then its trend is down and you invest in short- to intermediate-term fixed-income instruments until the trend turns positive.

In this way you always invest with the trend of the market.

Look at your investments monthly

Each month you use exactly the same test to determine if you should stay invested.

This means if the asset (for example the S&P 500 index) shows a positive excess return (return minus the Treasury bill rate) during the past 12 months, you stay invested.

If the prior 12-month excess return is negative, you sell the asset and invest in a short term bond fund.

How well does dual momentum perform?

Gary tested this dual momentum strategy over a 39 year period from October 1974 to October 2013.

This is what he did.

Each month he compared the S&P 500 index to the ACWI ex-U.S. index over the past year and selects whichever index has performed better. He then looked to see if the selected index has done better than U.S. Treasury bills. If it has, he invested in the index. If not, he invested in the Barclays U.S. Aggregate Bond Index.

He repeated this process every month from October 1974 to October 2013. During this time the strategy spent 41% of its time invested in the S&P 500, 29% in the ACWI ex-U.S., and 30% in aggregate bonds index.

Surprisingly low turnover only 1.4 times per year

On average, there were only 1.35 switches per year between these three assets, which means transaction costs were very low.

What were the returns?

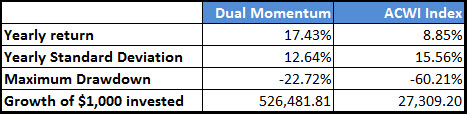

This table summarises the returns of the strategy compared to the index:

ACWI Index = MSCI ACWI Index (All Country World Index)

Source: Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk

As you can see over the 39 year period this strategy returned an average of 17.43% per year compared to the 8.85% of the ACWI Index over the same period.

The strategy was also a lot less risky compared to investing in the index as its maximum drawdown was only 22.7% compared to 60.21% of the ACWI Index and a return standard deviation of 12.64% (ACWI Index 15.56%).

Impressive results I am sure you will agree.

How you can use it in your portfolio

Dual momentum can be used in any market environment due to its adaptable nature.

Absolute momentum will let you participate in any market that has a positive trend and relative momentum will let you invest in the best performing assets for as long as the trends continues. When the trend disappears dual momentum will move your investments to cash before the change can do too much damage to your portfolio.

If you consider all the uncertainties when investing I am sure you will agree dual momentum investing is attractive.

How to implement it in your portfolio

First you need to decide over what past period you are going to look at to determine if the absolute momentum is positive.

In his book Gary used 12-months, which is also the best look back period found in the above research paper. However, if you are a more risk adverse you can use periods of three, six or nine months.

Next you have to decide where you want to invest.

If you invest in the US stock markets

If you want to invest in the US markets look if the return of the US S&P 500 ETF (SPY ETF) over the period (3 to 12 months) is greater than the US Treasury bill (T-Bill) rate which you can see here: US Treasury bill rates.

If the return of the SPY index is more than the T-Bill rate you can either:

- Buy the SPY ETF or

- For higher returns, use the screener to invest in one of the best investment strategies we have tested.

If the return of the SPY index is less than the T-Bill rate you sell all your stock market investments and:

- Buy the short term (1-3 year) US Treasury bond ETF (SHY ETF) or

- Stay in cash

If you want to invest in the European stock markets

If you want to invest in the European markets look if the return of the STOXX Europe 600 ETF (Stoxx 600 ETF) over the period (3 to 12 months) is greater than the Eurozone 3 to 12 month interest rate which you can find here: Eurozone interest rates.

If the return of the Stoxx 600 ETF is more than the three month Eurozone interest rate you can either:

- Buy the Stoxx 600 ETF or

- For higher returns, use the screener to invest in one of the best investment strategies we have tested.

If the return of the Stoxx 600 ETF is less than the three month Eurozone interest rate you can either:

- Buy the buy the short term (1-3 year) International Government bond ETF (SHY ETF) or

- Stay in cash

Dual momentum is an interesting strategy that is easy to implement, beats the market and limit your losses.

And it is a good strategy to follow even if you use (or am planning on using) one to the best performing investment strategies we have tested.

PS To find investment ideas based on the best investment strategies we have tested sign up here

PPS It is so easy to put things off why not sign up right now before it slips your mind

Sources:

Interview with Gary Antonacci on Momentum Based Investing

Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk

Optimal Momentum: A Global Cross Asset Approach

Risk Premia Harvesting Through Dual Momentum

Absolute Momentum: A Simple Rule-Based Strategy and Universal Trend-Following Overlay